https://www.leadsquared.com/wp-content/uploads/2020/10/Loan-origination-system-guide.jpg416800Preksha ABhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Preksha AB2020-10-31 10:57:342023-12-14 15:05:41Everything you should know about Loan Origination Systems

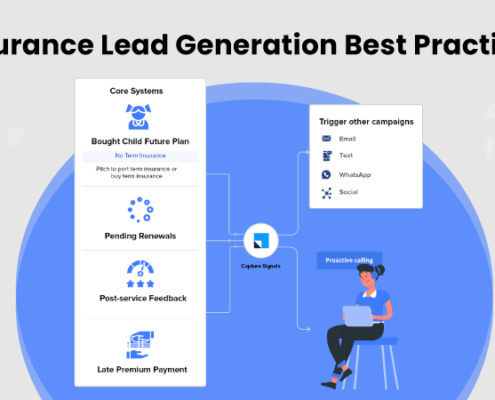

https://www.leadsquared.com/wp-content/uploads/2020/10/Loan-origination-system-guide.jpg416800Preksha ABhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Preksha AB2020-10-31 10:57:342023-12-14 15:05:41Everything you should know about Loan Origination Systems https://www.leadsquared.com/wp-content/uploads/2021/11/insurance-lead-generation-best-practices.png4501000Nidhi Agarwalhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Nidhi Agarwal2020-10-31 10:19:462023-11-08 15:07:01Insurance Lead Generation Best Practices: Do’s and Don’ts

https://www.leadsquared.com/wp-content/uploads/2021/11/insurance-lead-generation-best-practices.png4501000Nidhi Agarwalhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Nidhi Agarwal2020-10-31 10:19:462023-11-08 15:07:01Insurance Lead Generation Best Practices: Do’s and Don’ts https://www.leadsquared.com/wp-content/uploads/2021/11/improve-B2C-sales.jpg5451000Nidhi Agarwalhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Nidhi Agarwal2020-10-30 08:41:172023-12-11 19:26:39How to Improve B2C Sales: Tips for Sales Managers

https://www.leadsquared.com/wp-content/uploads/2021/11/improve-B2C-sales.jpg5451000Nidhi Agarwalhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Nidhi Agarwal2020-10-30 08:41:172023-12-11 19:26:39How to Improve B2C Sales: Tips for Sales Managers https://www.leadsquared.com/wp-content/uploads/2020/10/CRM-Software-Capabilities.jpg5001000Nidhi Agarwalhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Nidhi Agarwal2020-10-28 12:27:272023-12-12 10:21:12What are the key capabilities of CRM Software?

https://www.leadsquared.com/wp-content/uploads/2020/10/CRM-Software-Capabilities.jpg5001000Nidhi Agarwalhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Nidhi Agarwal2020-10-28 12:27:272023-12-12 10:21:12What are the key capabilities of CRM Software? https://www.leadsquared.com/wp-content/uploads/2021/11/banner-RE.jpg4501000Vivek Hariharanhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Vivek Hariharan2020-10-28 11:32:132023-06-08 14:25:30Residential Real Estate Outlook 2021

https://www.leadsquared.com/wp-content/uploads/2021/11/banner-RE.jpg4501000Vivek Hariharanhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Vivek Hariharan2020-10-28 11:32:132023-06-08 14:25:30Residential Real Estate Outlook 2021 https://www.leadsquared.com/wp-content/uploads/2021/11/mortage-loan-origination-software.jpg4501000Nidhi Agarwalhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Nidhi Agarwal2020-10-25 10:55:002023-12-22 11:44:23What is Mortgage Loan Origination Software?

https://www.leadsquared.com/wp-content/uploads/2021/11/mortage-loan-origination-software.jpg4501000Nidhi Agarwalhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Nidhi Agarwal2020-10-25 10:55:002023-12-22 11:44:23What is Mortgage Loan Origination Software? https://www.leadsquared.com/wp-content/uploads/2021/11/upcoming-lending-business-trends.jpg5001000Nidhi Agarwalhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Nidhi Agarwal2020-10-24 17:31:002023-12-13 19:02:20Lending Business Technology Trends 2024

https://www.leadsquared.com/wp-content/uploads/2021/11/upcoming-lending-business-trends.jpg5001000Nidhi Agarwalhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Nidhi Agarwal2020-10-24 17:31:002023-12-13 19:02:20Lending Business Technology Trends 2024 https://www.leadsquared.com/wp-content/uploads/2021/11/EduTech-Trends-Machine-Learning.jpg5001000Nidhi Agarwalhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Nidhi Agarwal2020-10-23 17:55:002023-12-22 11:46:08EdTech Sales Process Automation Guide

https://www.leadsquared.com/wp-content/uploads/2021/11/EduTech-Trends-Machine-Learning.jpg5001000Nidhi Agarwalhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Nidhi Agarwal2020-10-23 17:55:002023-12-22 11:46:08EdTech Sales Process Automation Guide https://www.leadsquared.com/wp-content/uploads/2021/11/sms-marketing.jpg626626Sarilya Jaiswalhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Sarilya Jaiswal2020-10-23 00:50:422023-12-22 11:47:40The Dos and Don’ts of Texting: SMS Marketing Best Practices

https://www.leadsquared.com/wp-content/uploads/2021/11/sms-marketing.jpg626626Sarilya Jaiswalhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Sarilya Jaiswal2020-10-23 00:50:422023-12-22 11:47:40The Dos and Don’ts of Texting: SMS Marketing Best Practices https://www.leadsquared.com/wp-content/uploads/2021/11/Digital-Loan-Management-System.jpg416800Preksha ABhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Preksha AB2020-10-22 17:29:522023-11-02 14:16:59A Complete Guide to Loan Management Systems

https://www.leadsquared.com/wp-content/uploads/2021/11/Digital-Loan-Management-System.jpg416800Preksha ABhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Preksha AB2020-10-22 17:29:522023-11-02 14:16:59A Complete Guide to Loan Management Systems https://www.leadsquared.com/wp-content/uploads/2021/11/what-is-Insurance-sales-funnel.jpg4501000Nidhi Agarwalhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Nidhi Agarwal2020-10-21 09:41:472023-12-11 17:51:14Decoding the Insurance Sales Funnel

https://www.leadsquared.com/wp-content/uploads/2021/11/what-is-Insurance-sales-funnel.jpg4501000Nidhi Agarwalhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Nidhi Agarwal2020-10-21 09:41:472023-12-11 17:51:14Decoding the Insurance Sales Funnel https://www.leadsquared.com/wp-content/uploads/2021/11/exclusive-life-insurance-leads.jpg4501000Nidhi Agarwalhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Nidhi Agarwal2020-10-21 09:28:302024-03-06 22:35:31Life Insurance Lead Generation Ideas: How to find exclusive leads?

https://www.leadsquared.com/wp-content/uploads/2021/11/exclusive-life-insurance-leads.jpg4501000Nidhi Agarwalhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Nidhi Agarwal2020-10-21 09:28:302024-03-06 22:35:31Life Insurance Lead Generation Ideas: How to find exclusive leads? https://www.leadsquared.com/wp-content/uploads/2021/11/healthcare-crm-for-hospitals-1.png432598Vivek Hariharanhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Vivek Hariharan2020-10-20 14:36:402023-11-24 16:38:31CRM in Healthcare Industry: 12 Practical Benefits

https://www.leadsquared.com/wp-content/uploads/2021/11/healthcare-crm-for-hospitals-1.png432598Vivek Hariharanhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Vivek Hariharan2020-10-20 14:36:402023-11-24 16:38:31CRM in Healthcare Industry: 12 Practical Benefits https://www.leadsquared.com/wp-content/uploads/2021/11/features-benefits-of-marketing-automation.jpg4501000Nidhi Agarwalhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Nidhi Agarwal2020-10-20 11:52:112024-01-24 17:14:32What are the Features and Benefits of Marketing Automation?

https://www.leadsquared.com/wp-content/uploads/2021/11/features-benefits-of-marketing-automation.jpg4501000Nidhi Agarwalhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Nidhi Agarwal2020-10-20 11:52:112024-01-24 17:14:32What are the Features and Benefits of Marketing Automation? https://www.leadsquared.com/wp-content/uploads/2021/11/Mortgage-software-benefits.jpg416800Nidhi Agarwalhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Nidhi Agarwal2020-10-19 18:30:482023-12-22 11:52:17Mortgage Software for Effective Loan Management

https://www.leadsquared.com/wp-content/uploads/2021/11/Mortgage-software-benefits.jpg416800Nidhi Agarwalhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Nidhi Agarwal2020-10-19 18:30:482023-12-22 11:52:17Mortgage Software for Effective Loan Management https://www.leadsquared.com/wp-content/uploads/2021/11/Onboarding-System-for-Field-Sales-Agents.jpg416800Nidhi Agarwalhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Nidhi Agarwal2020-10-18 11:38:022023-12-22 11:53:32Why is online onboarding system necessary for field sales agents?

https://www.leadsquared.com/wp-content/uploads/2021/11/Onboarding-System-for-Field-Sales-Agents.jpg416800Nidhi Agarwalhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Nidhi Agarwal2020-10-18 11:38:022023-12-22 11:53:32Why is online onboarding system necessary for field sales agents? https://www.leadsquared.com/wp-content/uploads/2021/11/Using-Automation-to-Turn-Prospects-into-Customers.jpg4001000Shibani Royhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Shibani Roy2020-10-15 14:00:002023-11-06 18:30:11How Can Chatbot and CRM Help Gain More Customers?

https://www.leadsquared.com/wp-content/uploads/2021/11/Using-Automation-to-Turn-Prospects-into-Customers.jpg4001000Shibani Royhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Shibani Roy2020-10-15 14:00:002023-11-06 18:30:11How Can Chatbot and CRM Help Gain More Customers?  https://www.leadsquared.com/wp-content/uploads/2021/11/Vendor-Onboarding-software-feature.png6731000Nidhi Agarwalhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Nidhi Agarwal2020-10-14 09:00:002023-12-22 11:55:05Understand Onboarding Automation

https://www.leadsquared.com/wp-content/uploads/2021/11/Vendor-Onboarding-software-feature.png6731000Nidhi Agarwalhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Nidhi Agarwal2020-10-14 09:00:002023-12-22 11:55:05Understand Onboarding Automation https://www.leadsquared.com/wp-content/uploads/2021/11/Real-estate-CRM-1.jpg4501000Vivek Hariharanhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Vivek Hariharan2020-10-13 20:21:562023-12-22 11:58:197 Benefits of using CRM to Accelerate Real Estate Sales

https://www.leadsquared.com/wp-content/uploads/2021/11/Real-estate-CRM-1.jpg4501000Vivek Hariharanhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Vivek Hariharan2020-10-13 20:21:562023-12-22 11:58:197 Benefits of using CRM to Accelerate Real Estate Sales https://www.leadsquared.com/wp-content/uploads/2021/11/enrollment-management-strategies.jpg6001000Nidhi Agarwalhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Nidhi Agarwal2020-10-13 17:54:232023-12-22 12:28:57Digital Enrollment Management Strategies for Colleges

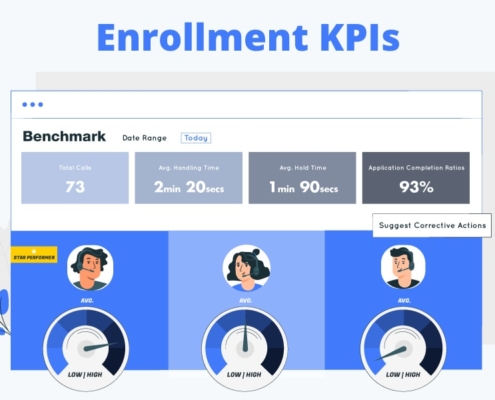

https://www.leadsquared.com/wp-content/uploads/2021/11/enrollment-management-strategies.jpg6001000Nidhi Agarwalhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Nidhi Agarwal2020-10-13 17:54:232023-12-22 12:28:57Digital Enrollment Management Strategies for Colleges https://www.leadsquared.com/wp-content/uploads/2021/11/Enrollment-Management-KPIs.jpg6001000Nidhi Agarwalhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Nidhi Agarwal2020-10-13 10:35:002024-03-07 00:12:435 Important KPIs to track in your enrollment management strategic plan

https://www.leadsquared.com/wp-content/uploads/2021/11/Enrollment-Management-KPIs.jpg6001000Nidhi Agarwalhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Nidhi Agarwal2020-10-13 10:35:002024-03-07 00:12:435 Important KPIs to track in your enrollment management strategic plan https://www.leadsquared.com/wp-content/uploads/2021/11/Edtech-sales-strategy.jpg10801920Vivek Hariharanhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Vivek Hariharan2020-10-12 16:28:452023-11-15 16:35:28Edtech Sales & Marketing Hacks to Increase Enrollments

https://www.leadsquared.com/wp-content/uploads/2021/11/Edtech-sales-strategy.jpg10801920Vivek Hariharanhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Vivek Hariharan2020-10-12 16:28:452023-11-15 16:35:28Edtech Sales & Marketing Hacks to Increase Enrollments https://www.leadsquared.com/wp-content/uploads/2021/11/Lending-software-Benefits.jpg6001000Nidhi Agarwalhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Nidhi Agarwal2020-10-12 13:51:012024-03-06 23:36:55How Lending Software Can Increase Operational Efficiency

https://www.leadsquared.com/wp-content/uploads/2021/11/Lending-software-Benefits.jpg6001000Nidhi Agarwalhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Nidhi Agarwal2020-10-12 13:51:012024-03-06 23:36:55How Lending Software Can Increase Operational Efficiency https://www.leadsquared.com/wp-content/uploads/2021/11/CRM-FOR-INSURANCE-AGENTS.jpg416800Meenu Joshihttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Meenu Joshi2020-10-10 10:20:452023-12-22 12:32:52CRM for Insurance Agents: How Agents Can Grow Their Practice

https://www.leadsquared.com/wp-content/uploads/2021/11/CRM-FOR-INSURANCE-AGENTS.jpg416800Meenu Joshihttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Meenu Joshi2020-10-10 10:20:452023-12-22 12:32:52CRM for Insurance Agents: How Agents Can Grow Their Practice