FINANCE

20 Fintech Trends That Will Shape the Future of Finance in Southeast Asia

Contents

Fintech startups are changing the way we do business and complete transactions. Instead of carrying a wallet full of cash and cards, you only need a smartphone and one of the many fintech apps available.

Let’s take a closer look at fintech and how these trends will change everything for the future of finance in Southeast Asia.

Fintech is a technology built for financial activities. Fintech startups typically distribute these tools as smartphone apps. You can access them with only an internet connection and an email address.

Fintech tools assist people with everyday finance, including money transfers, making deposits, applying for credit, and managing investments. All without the need for a traditional banking institution (or any humans at all).

Fintech puts banking and financial services in the palm of your hand. And while some parts of the world are adopting smartphones and banking apps more quickly, Southeast Asia is gaining steam.

One of the critical factors for fintech growth is that banks and investment firms are investing heavily in fintech startups. The global fintech market is expected to grow at a rate of 20% and reach $305 billion by 2025.

Only 53% of Southeast Asia’s population are smartphone users. Compare that to 80% of Europeans, and you may wonder if fintech is a passing trend or a global shift.

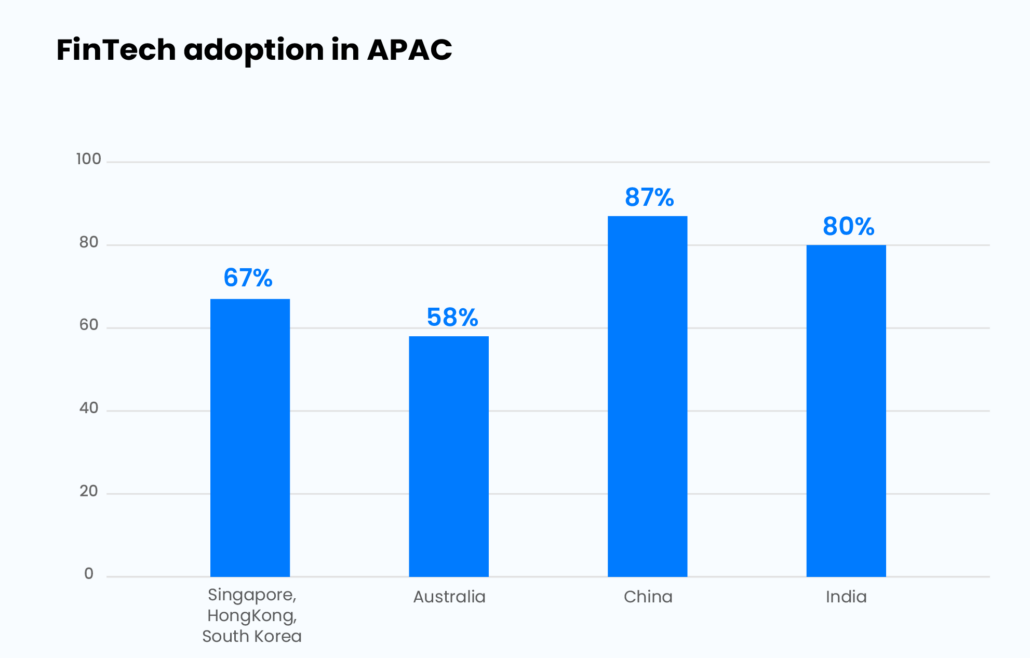

But in only two years since the onset of the COVID-19 pandemic, fintech usage has doubled in key Asia-Pacific markets. For example, Singapore, Hong Kong, and South Korea have 67% fintech adoption, Australia has 58%, China 87%, and India 80%.

Here are some examples of fintech trends that are changing everything:

SEA-based fintech companies already make it easier for people to manage their money in daily life, and now they are making it even easier to spend and collect funds. Although digital banking has been around for a decade, fintechs are finding new ways to enhance these services.

For example, neobanks are banks that operate online only without a physical location. These fintech apps allow users to open an account, transfer funds, open a credit account, buy crypto, get a loan, and even secure short-term financing.

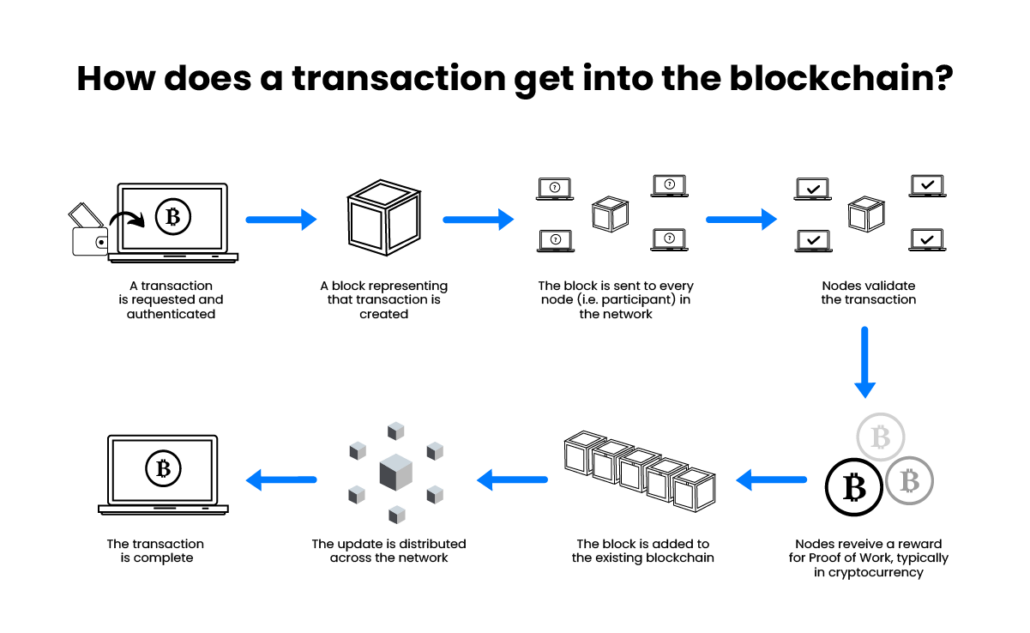

Blockchain acts as a digital ledger that tracks every move an asset makes, no matter how many wallets it passes through. It’s also the power behind crypto. And since the digital ledger is becoming the new way to keep track of digital transactions, blockchain has several uses for fintech.

In addition to crypto, NFTs and decentralized finance (DeFi) apps also use blockchain to buy, sell, trade, and power the digital asset market.

What does the IoT have to do with finance? Well, it’s changing how fintech companies from around the world look at and understand financial information. Sensors and other devices can monitor ATMs and keep track of micro-payments like monthly subscriptions. They can also encourage contactless payments.

Anything can be an IoT device; it just needs to have a way to connect to the internet and transfer information from one place to another. Fintech tools can use this technology to create connected credit and debit cards that interact with almost no processing time. The possibilities are endless.

In a traditional setting, a physical bank is where you will go to get financial advice, set up new accounts, and get a loan. Video banking is another way that fintech companies are changing the way we think about finance.

In addition to creating the neobank market, fintechs also use video to enhance their banking services. Video banking uses video calling technology and facial recognition to bring a familiar feel to digital banking.

AR and VR are not just for gaming. These technologies also have promising uses for Southeast Asian fintech companies as well. For example, you might need VR goggles to access a bank that exists in the metaverse. Or perhaps fintechs can use AR to enable digital payments.

AR and VR for fintech are still evolving, but some companies are already experimenting. Back in 2016, Goldman Sachs Research expert Heather Bellini predicted that virtual and augmented reality would be an $80 billion industry by 2025. They also hinted that financial technology could be the catalyst for such massive growth.

Imagine if you could pay your bills just by using your voice. “Hey Alexa, pay the electric bill.” That sounds easy, doesn’t it? Well, now you can!

Voice-enabled technology lets people use their smartphones or a digital assistant like Siri, Alexa, or Hey Google to use their voice to interact with the digital world. There are rumors that fintech startups are looking for ways to implement voice-enabled technology to make contactless and digital payments.

A smart contract is a program that runs on blockchain technology. When certain conditions are met, the smart contract runs automatically. In finance, smart contracts can be used to automate agreements without a third party like a bank or loan officer. That means buyers and sellers can securely connect with a legal agreement without banking involvement.

Smart contracts are already popular among crypto and blockchain users, but fintechs are also starting to get involved. Smart contracts powered by DeFi fintech apps could become the norm in the future. Imagine that you need a home loan. Instead of going to a bank, you obtain a loan based on a smart contract and have the money in minutes or less.

Right now, 90% of DeFi lending is done in stablecoins. As more governments navigate the crypto space by creating their own digital tokens, smart contracts could quickly replace loan officers.

RPA automates repetitive tasks without the help of humans. It can take over tedious tasks that bog down productivity, giving humans more time for other activities. And in the financial services industry, there is no shortage of tedious work.

Fintechs are making banking accessible to consumers and better for workers, too. Using RPA, workers have less monotonous work to do, and consumers receive their services faster than ever. Chatbots in banking are a great example of RPA in action.

We already discussed how fintechs could change everything with connected credit cards and IoT devices, but what about virtual cards? Instead of putting a computer in the card, a virtual card lives in the digital world. There is no physical card, only a credit card number, CVV, and expiration date.

A virtual card is similar to a digital wallet like PayPal. But where digital wallets store physical card information, a virtual card doesn’t exist anywhere else. However, you can still use it online, just like a regular debit or credit card.

Some ways that fintech is changing the world haven’t fully been realized but are still on the horizon. Autonomous finance is a system of connected machines and devices that don’t need humans to perform financial transactions. Though we haven’t made it to autonomous finance yet, technology like smart contracts shows us what the future of fintech could look like.

The Southeast Asian-based financial services industry covers a wide range of money-related services. That includes savings, investments, and retirement. Fintechs are also changing how we handle more complex transactions with programs dedicated to wealth management. They call it WealthTech.

Some of the biggest names in tech are already involved in creating the tools and infrastructure required to perform wealth management activities. And now, fintechs are changing the game again. Robo-advisors, smart contracts, and investment trading platforms are all making wealth more accessible to consumers.

Cybersecurity is an ongoing problem. And with fintech, it’s even more important to consider security. Protecting your money and other financial assets is a serious concern. But fintechs are experimenting with new security models to make neobanks and financial services safe to use.

Biometric security uses things like fingerprints, retina scanning, and facial recognition to authenticate users. Since biometrics are unique to their specific humans, it would be very difficult for a hacker to infiltrate your accounts.

Without AI and ML, fintech would just be online banking. But automation allows fintechs to use risk assessment and management tools, forecasting, and data management to give their products more intuitive features. Intuitive features make fintech apps easier to use and more convenient for customers.

For example, robo-advisors can automatically manage investment portfolios based on market trends and your pre-programmed parameters. Fintechs can also use ML to learn and predict customer behavior.

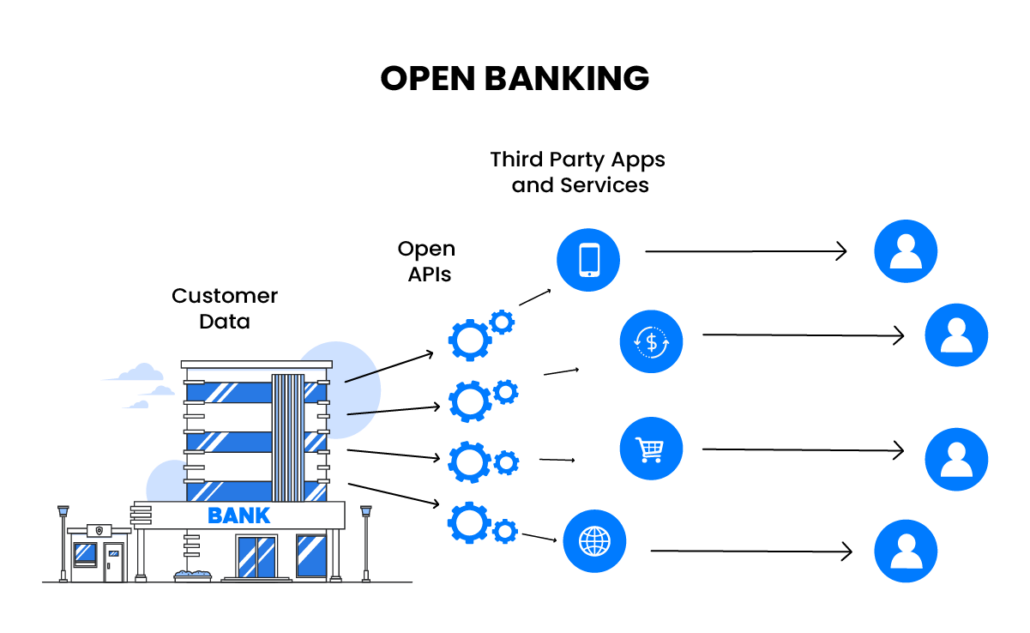

Open banking means that banking activities aren’t limited to banks. Neobanks powered by fintechs have paved the way for open banking to exist. Since neobanks are essentially apps that are a bank (rather than a bank that has an app), can anyone provide banking services? Open banking says yes!

It means that banks and fintechs can use third-party APIs to create their own banking platforms. As long as you are willing to trust an organization with your financial information, they can bank you through open banking. This makes banking technology more accessible and can even make it easier to do things like getting a loan.

It’s no secret that cybersecurity is an issue for all types of tech companies. But people who use fintechs have a lot to lose (virtual money in a virtual bank = cybersecurity nightmare.) However, fintech companies are redefining cybersecurity.

Blockchain, secure access service edge (SASE), multi-cloud data storage, and decentralization are all important cybersecurity advances created with fintechs in mind. In the future, fraud management, anti-money laundering, and passwordless authentication may all be solved by fintechs.

Big data keeps on getting bigger. Companies worldwide utilize big data to make predictions and business decisions and forecast future trends. But regulations worldwide make it difficult to share this data across borders.

DeFi apps powered by fintech change all of that. Decentralized data can connect platforms across borders for the most accurate reporting and up-to-date forecasting. It even has the power to predict market fluctuations, potential growth, and other financial activities.

RegTech is a technology that is used to keep track of regulatory compliance. These solutions use automation to monitor and report on things that affect financial institutions.

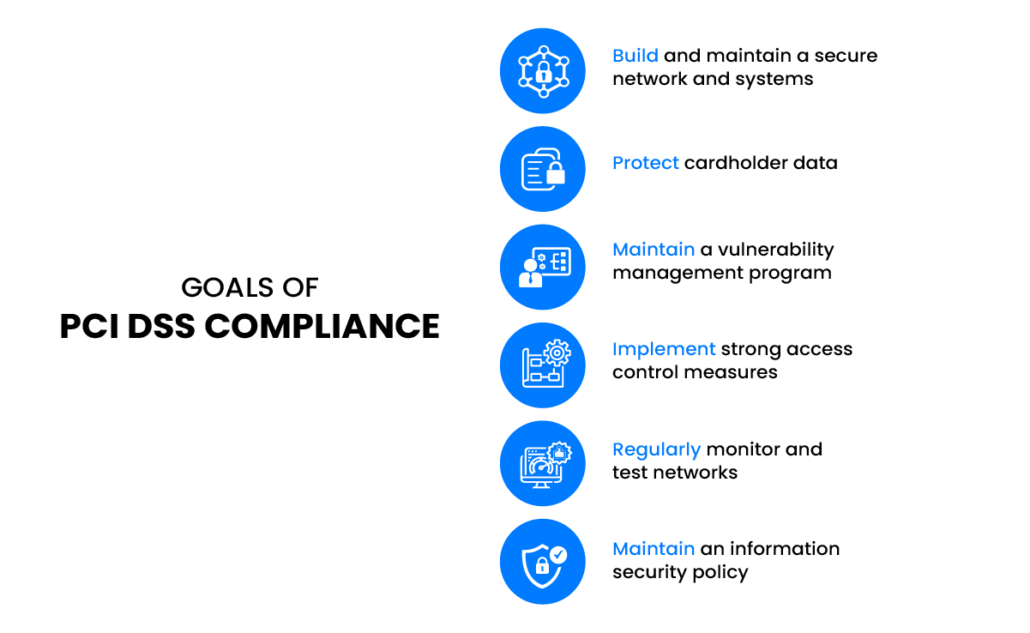

This is especially important since fintech is disrupting everything we know about banking. RegTech makes it easier to connect businesses with their regulating bodies so that they can seamlessly transfer data, monitor for compliance such as keeping in line with the PCI compliance standards, and keep an eye on financial crimes.

Gamification, or turning boring things into a game, is popular way businesses engage their customers. But what does it have to do with fintech? Fintechs are using games to encourage customers to make good financial choices. For example, games with rewards help people track their spending and achieve savings goals without stress.

Gamification makes finance fun and engaging. Instead of being stressed out about navigating new technologies and asset classes while the economy evolves around us, gamification can add a layer of interest and relaxation to paying your bills.

Quantum computing is no longer a far-off dream of the future. Sycamore is the name of Google’s quantum processor, the fastest machine on the planet. They recently developed a quantum virtual machine that allows users to develop using quantum technology from anywhere in the world.

For fintech, this opens up new doors yet to be discovered. In addition to providing banking services faster than ever, quantum computing can also enhance security and privacy, improve trading algorithms, and settle transactions in the blink of an eye.

It’s almost impossible to participate in the economy without a bank account, but unfortunately for many, landing a bank account is out of the question. Over 70% of Southeast Asia is either unbanked or underbanked. This excludes them from things like applying for loans, getting a credit card, or getting insured.

Some regulators, like the Insurance Bureau of Canada (IBC), have policies to help those without credit. But in Asia, there is still a lot of deregulations to do. Fintechs are making it easier for everyday people to access banking activities online. Encouraging people to take out loans and make payments over time helps build their credit and improve their quality of life.

Fintech is changing everything. It’s changing how we bank, how we buy, and how we save for retirement. There are powerful technologies behind fintech pushing humanity toward a more connected and available economic system. Digital transformation in the financial arena is focused on fintech.

Fintech is breaking down barriers to financial services. Plus, it’s also innovating cyber security and fraud prevention tools. These are just a few fintech trends that are changing the world as we know it. What do you think is next on the horizon for fintech?

Enter your details and we'll send you a quick confirmation email to verify your address.

Key Points to Achieving and Integrating a Comprehensive Student Journey Map

Key Points to Achieving and Integrating a Comprehensive Student Journey Map