LENDING

5 Ways to Improve Debt Collection Through Automation

Contents

Debt collection is at the forefront of the lending industry as it directly supports an organization’s revenue. Growing consumerism is promoting debts creating a promising opportunity for lenders. But at the same time, recovering bad debts, which is also increasing concurrently, raises serious concerns among Collectors.

For example, in the United States, consumer debt has increased nearly by USD 2.3 trillion (2019) since the Great Recession in 2009. The COVID-19 pandemic is making it even more difficult to recover debts. Debt collection practices are already governed by stringent laws. The state officials and regulators are further imposing restrictions on debt collection to minimize the economic burdens stemming from COVID-19 on consumers.

Regardless, with the right process and tools, businesses can manage accounts and reduce Days Sales Outstanding (DSO) effectively.

The time spent chasing after default cases is, of course, a major overhead in the lending sector. However, loan recovery also delays because of internal collection process challenges like:

A straightforward solution to all these challenges is automating the debt collection process. It starts from identifying the debtors to the final settlement. One of the prime enablers of automation in loan recovery is debt collection CRM that streamlines the entire collections process, including integrating payment gateways and communicating with customers. It can enhance personalized engagement with clients and increases agents’ productivity. Businesses can see immediate ROI soon after implementing the system.

Automation improves both – the debt recovery time and efficiency of the collection process. In any automated debt management system, the borrower, collection agent, and analytical insights are at the core. However, for now, let’s focus on the debt collection aspect of loan management and how digital solutions are making it more efficient.

The Bureau of Consumer Financial Protection received approximately 75,200 debt collection complaints in December 2019. Out of these, 45% of the complaints were made on attempts to collect debts not owed. Most of the consumers who lodged the complaints were the victims of identity theft.

A mistake in the borrower’s profile validation or losing the track of the borrower between the loan sanction and recovery period could lead to such right-party contact issues. Thus, maintaining a consolidated and updated borrower profile is essential.

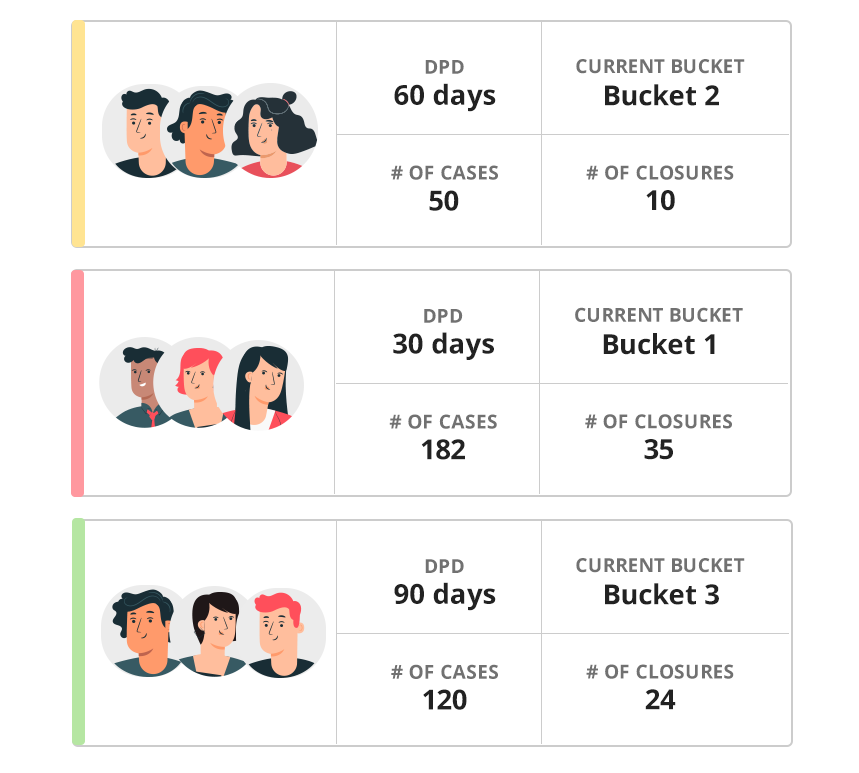

Based on the loan type, the amount owed, repayment date, occupation, and location parameters, borrowers can be segmented into different loan buckets. Segmentation helps in prioritizing cases.

Another problem that lenders face is of organizing information from different sources. Collections CRM can integrate with several information sources like CIBIL, Experian, and even social profiles and automatically update them in a centralized system. This saves the collector’s efforts in switching from multiple systems to derive a debtor’s information. Integrating Lending CRM with third-party applications like IVRs, Telephony services, and collection software can make the system even more efficient. For example, if there is an inbound telephonic call, an automation system in place can route it to a suitable agent in a round-robin manner.

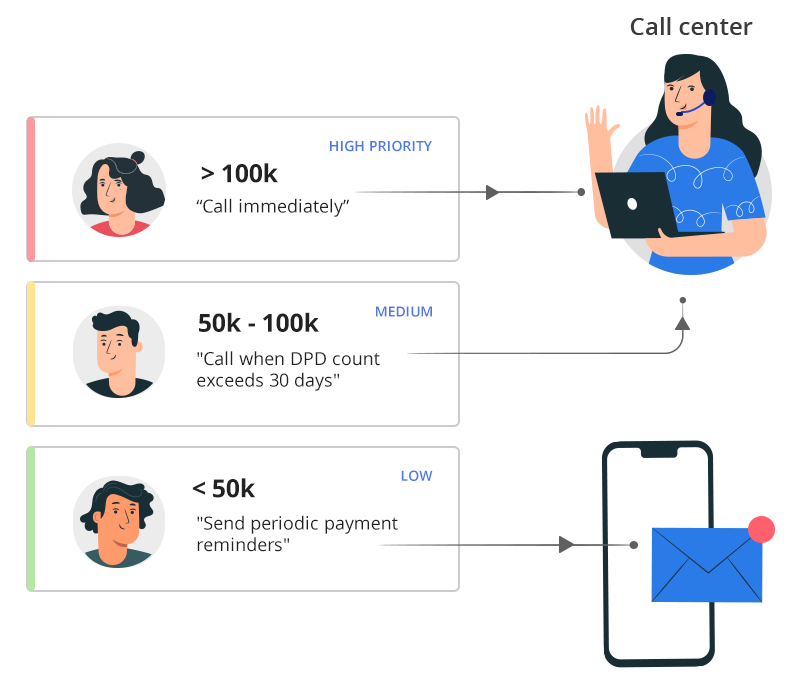

CFOs, credit managers, and collectors constantly focus more on accounts that need immediate attention. For instance, the law requires settling the disputed cases within 90 days of becoming apparent to the company. Else, the company might have to bear the loss. Thus, prioritizing delinquent cases that are closer to DPD (Days Past Due) is crucial.

Prioritizing individual cases manually can be time-consuming. It is also prone to errors. Debt Collection software can assign priorities to accounts based on the borrowers’ profile information including – DPD, asset classification, due amount, product type, delinquency bucket classification, wilful defaulter, and fraud identification.

Depending on the organization’s debt collection process, collection management systems can allocate an account to a call center, in-house team, field agent, or a third-party collection agency. It can also send reminders to agents to follow up with borrowers, ensuring timely communication.

The collections department usually evaluates the agent’s performance based on the following 5 KPIs (Key Performance Indicators):

Lenders acknowledge that the inability to track their field agent’s activities on the field is a pressing concern for them. For example, sometimes loan recovery fails because the collector isn’t putting the right efforts in contacting the debtor. Collection System Automation can detect and prevent your agents from signing-in from a fake location. Geofencing tasks can also help prevent fraudulent record entries.

There was a time when collectors used to carry a briefcase that contained a copy of borrower’s documents, notepad, legal paperwork, and more. Now, the mobile phone has become the briefcase of information and, in fact, more than that. Collectors can easily carry a mobile phone to a remote location, contact the borrower, and access the guarantor’s information if required.

Mobile collection software helps collectors to remain productive while being on the field. Reminder notifications, day planner, and route guidance are some of the sought-after features that impact productivity. It also lets collections agents keep a tab on their pending tasks on their mobile app.

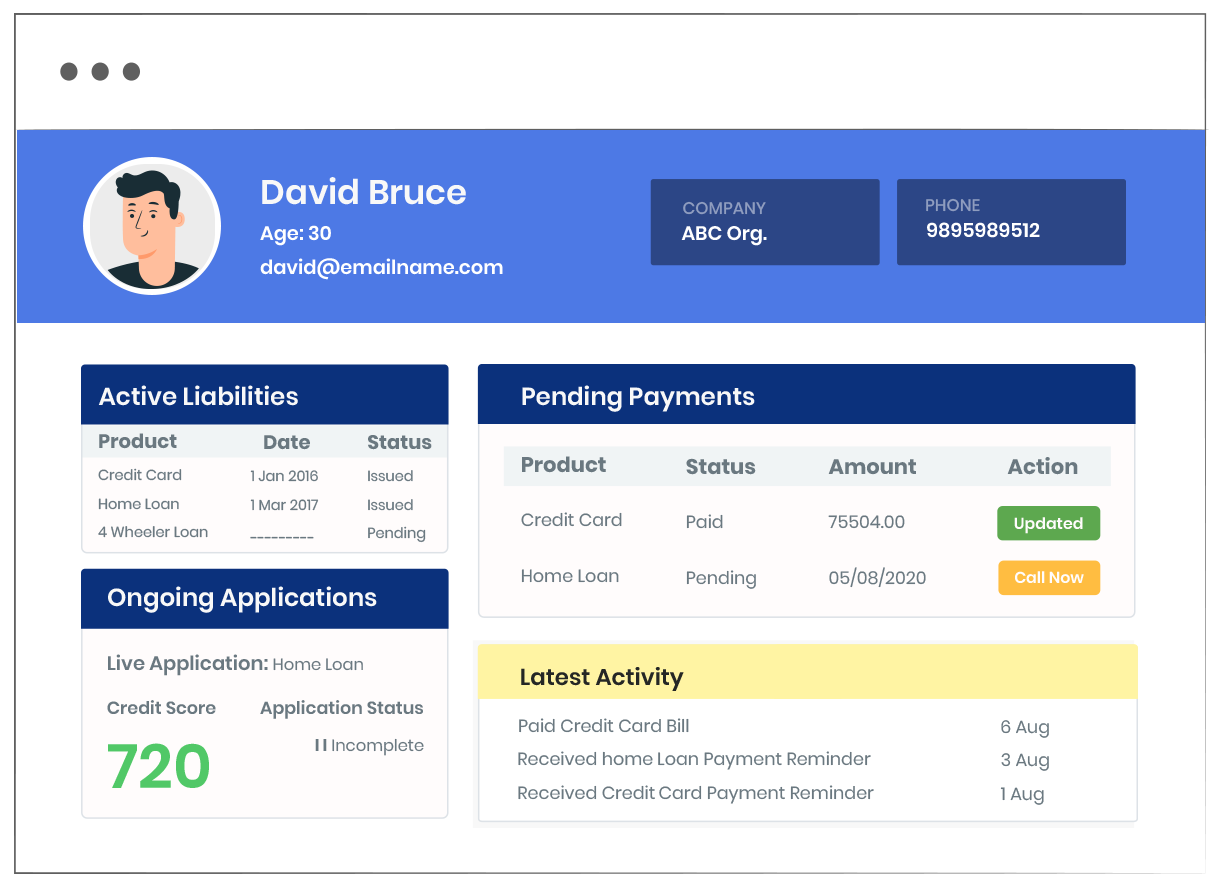

Data-driven insights on customers, collection efficiency, and team performances can help decision-makers evaluate ROI (Return on Investment) and eliminate bottlenecks from the collection funnel.

Reports on the number of debts recovered, intends to pay, non-responsive debtors, and the average time required for the debt recovery brings the teams in sync about the overall recovery performance – avoiding duplication of efforts. This way, every stakeholder is aware of the defaulter’s stage of repayment.

With smart dashboards, actionable insights on borrower profiles, agent performances, active liabilities, pending payments, ongoing payment activities, and more are at disposition for leaders.

Even though organizations have data points from loan defaulters, they fail in using them effectively. As a result, when organizations want to collect the bad debt, they don’t have the right set of tools and channels for delinquent clients. Some organizations fall into a dangerous spiral by collecting too little information as well.

Leveraging automation can make debt collection more efficient and reduce compliance litigations. To a great extent, debt collection automation system can break through the siloed infrastructure and legacy systems.

A practical solution to automating the collection process is using debt collection software or collections CRM that allows lenders to track and follow-up with debtors efficiently, predict and prioritize debt recovery, and enable faster collections. It can streamline the collection process across Financial Institutions like Banks and NBFCs, Collection Agencies, Healthcare, Government, Telecom, Real Estate, and Retail and handle a variety of loans like credit card debt, medical bills, student loans, mortgage, and auto loans.

Read more about how debt collection software helps in achieving recovery automation.

Debt recovery or debt collection is the process of following up with individuals or businesses to recover the owed sum of money.

There are several methods that lenders deploy to recover loans from borrowers. Lenders allocate cases to call centers and/or third-party collection agencies, or even sell debts at loss.

By prioritizing cases based on trackable metrics and investing in collection agents’ productivity, businesses can improve account receivable collection. Lenders can use Debt collection software to automate their loan recovery processes.

The plan to pitch and recover the sum owed by the borrower is known as debt revenue recovery strategy. It encompasses the lender, borrower, collection agent, and data-driven analytics.

Enter your details and we'll send you a quick confirmation email to verify your address.

Debt Collection CRM Features Checklist

Debt Collection CRM Features Checklist