LENDING

A Guide to Choose The Best Debt Collection Software in 2025

Contents

Over recent years, customers have changed the way they interact with their service providers. Now, they bank on convenience, user-friendliness, stellar customer support, and quick solutions to their problems. Take the lending industry, the need for quicker loan disbursals and POS financing like BNPL skyrocketed as new age customers prefer all things digital.

While disbursing loans can seem relatively quicker, debt collection, on the other hand, is challenging and time-consuming. Debt collection challenges include keeping up with regulatory changes, ensuring customer data security, accessing current debtor contact information, and establishing contact with debtors. This is where debt collection software comes in to keep track of defaulters, avoid bad debts, and enable faster recovery.

While most financial institutions have software to digitize different stages of the collections process, they’re often in silos, with data unavailable in a centralized fashion. An end-to-end debt collection software can be pivotal in automating the debt collection process and optimizing processes.

It streamlines the debt collection workflow for financial businesses while improving the efficiency of sales teams. For example, Canadian Customer Debt Relief (CCDR), Canada’s 4th largest Debt Collection and Management Organization, witnessed a net increase of 60% in debt collection productivity with debt collection software.

A debt collection software is a powerful tool to help streamline and automate the collection process and eliminate the chances of manual errors. It positively impacts debt recovery rate by:

Most lenders depend on third-party collection agencies to manage the collection process. But, this can be risky because businesses lose all control over customer experience and face operational issues such as delays in debt reconciliation. Whereas debt collection software in this context highlights all these errors as they arise and provide you with complete visibility throughout the collection process. Typically, a collection software integrated with ERP and loan management systems covers the overall debt management process.

Let’s look at a more few collections-related challenges that you can eliminate with debt collection software.

Customers who have outstanding loan amounts are frequently contacted by collection teams to initiate debt recovery. However, most customers may dodge communication in these instances. This can make it tough for collection agents to get in touch with customers for 30 days or even longer.

A debt collection software can digitize workflows and streamline customer engagement. After an initial round of communication, the subsequent outreach can take place via automated emails and messages so that agents can focus on high-risk customers who are much farther in the collections cycle.

Outstanding payments and debts written off as bad debts can impact cash flow.

From an analytical point of view, it highlights loopholes in the collection process and other internal inefficiencies that hint that money is being pumped out faster than it’s coming in.

Digital outreach with constant reminders make way for faster debt recovery and software-induced automation cuts down operational costs.

As the number of high-risk accounts increase, the manual work and subsequent errors that salespeople may make also shoots up. Task-based automation streamlines routine activities and helps agents prioritize tasks based on the risk involved for every account. This can positively impact productivity and output.

Being empathetic is crucial to establish strong customer relationships. Salespeople need to be consistent with their follow ups, but a high number of outbound calls, emails, and messages can be overwhelming from a customer’s point of view.

While automated communication can be used in the initial stages of the debt recovery process, customers must be given the liberty to make payments through self-service portals. For further stages, reminders to agents can be sent for follow-up. Debt collection software helps you plan each stage of customer engagement and simplifies it for the customer and the collector.

In 2019, prior to the COVID-19 pandemic, the average collection rate with traditional methods of debt recovery was below 20%—the lowest it had been in 25 years, according to Ernst and Young. This makes a strong case to assess the value that digitized debt collection adds by streamlining tasks with automation, adopting self-service portals, and accessing dynamic reports and analytics, etc.

Here are a few business instances to understand why debt collection software is more of a ‘need’ than a ‘want’.

At any point when the debtor is unable to pay the money that they owe, it is written off as bad debt. These irrecoverable debts generally occur when lenders are unable to segment borrowers based on credit risk and financial portfolios prior to disbursing loans. Other instances that result in bad debt are when collectors are unable to recover debts due to tracking errors that arise with legacy technology.

But, debt collection software can easily identify cases of high risk. This gives better clarity for collectors to focus their time on cases that have a high probability of bad debt.

With AI, debt collection software can automatically qualify debtors based on behavioral insights and potential risks. This further gives lenders insight into the credit risk involved, and how they can structure payment terms to ensure faster debt recovery.

Most financial institutions use legacy technology that stores their data in silos. This can be a setback when multiple teams are involved throughout the collections process leading to an incomplete picture of the borrower’s journey. Debt collections software centralizes data and establishes a single source of truth to enable better customer journeys and mitigate any potential risks.

A customer’s financial data is confidential and sensitive in nature. In a time when customers are more aware of data protection and are conscious of giving consent, financial institutions must ensure that all security standards are met.

Debt collection software acts as a secure platform to store and manage customer information, prevent the risk of data breaches and instances of non-compliance penalties. In terms of compliance, that differs from one geography to another, the BFSI space is a highly regulated one. For instance, the Consumer Financial Protection Bureau (CFPB) bounds debt collectors in the United States with Regulation F, which curbs collectors from excessively contacting borrowers in a specific window of time with the intent to recover debts. Debt collection software in this context can help alert potential compliance violations, send alerts when there are changes in regulations, etc.

Automating tasks along the collections process can free up your agent’s time to focus on critical cases. For example, first-level queries can be handled by collection bots. Or you can set up timely reminders on your debt collection software if a certain borrower needs further personalized follow-up to recover debts.

Digitizing collections process also allows you to gain analytical insights that come in handy across the hierarchy of agents and management. For instance, the head of collections can easily access data on timely loan fulfillment and the rate of bad debt. Similarly, managers can find out the number of appointments the agents have managed to complete in a day. These reports align collection strategies for different borrower segments to strategize and improve their operations.

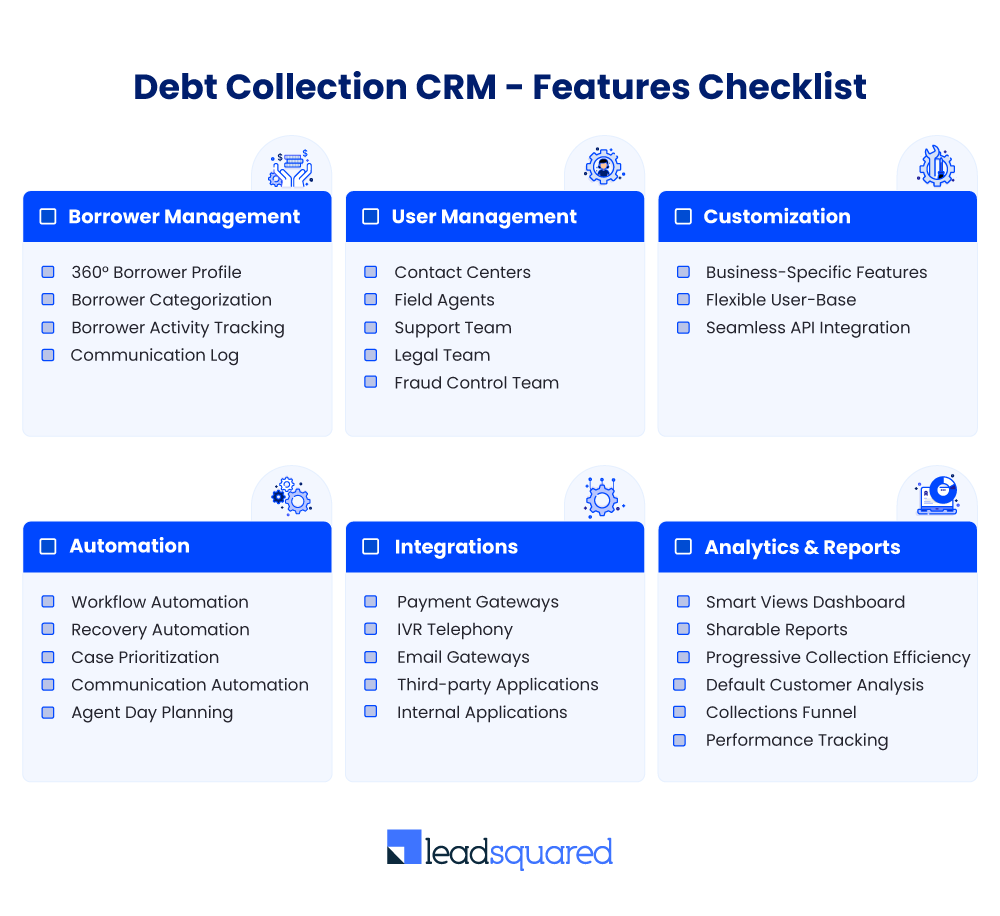

To make the decision of buying a debt collection software easier, here’s a handy checklist to guide you through the features you should look for:

You can also download this checklist to share it with your team: Feature Checklist to choose a Debt Collection CRM.

Financial institutions maintain a portfolio of their borrowers. Based on the borrower persona and collection strategy, lenders assign cases to call centers or resolution agencies.

Usually, debt collection software is customizable to the lender’s specific requirements. It might also have different offerings for accounts receivable and collection on bad debts. However, you can expect features like borrower management, recovery automation, and analytical insights in most of the debt collection platforms.

Having consolidated borrower information helps agents strike a meaningful conversation with them. This profile also covers all the stages in the borrower lifecycle. Example: borrower onboarding, segmentation, debt recovery prediction, and case closure. Collection CRMs can access borrower information from several data exchange APIs. LOS, CIBIL, Experian Hunter, Perfios, NetBanking Connect, and PDF Statement Analyzer are some of them. This information strengthens the borrowers’ profile information for future use. Debt collection software also allows importing existing and older cases from other software.

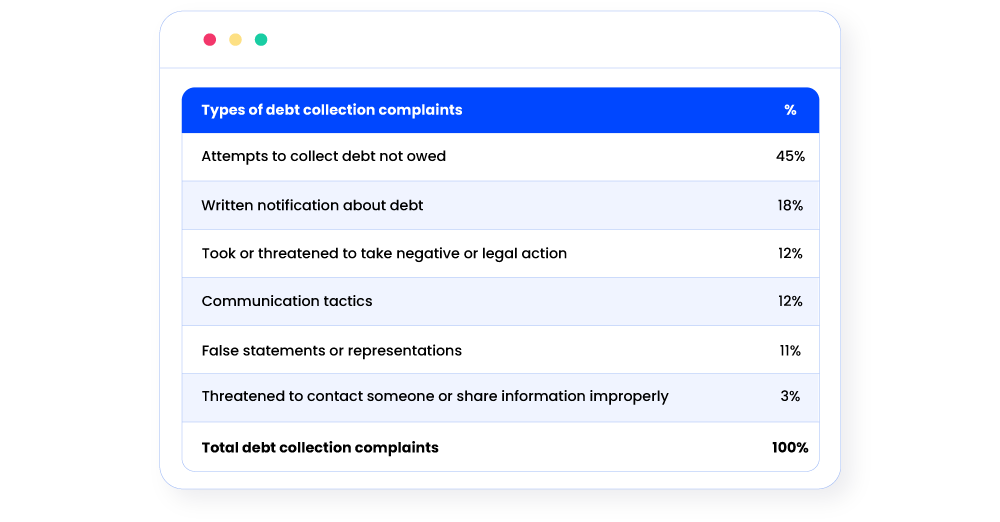

Maintaining an accurate borrower profile is crucial for businesses to avoid the repercussions of chasing after wrong profiles. For instance, The Bureau of Consumer Financial Protection of the United States mentions receiving a large volume of complaints on an attempt to collect debt not owed.

Collections software segments your borrowers into different debt buckets. It uses DPD (Days Past Due), credit repayment history, the amount due, and repayment intent for segmentation. The system first identifies the number of debtors in each bucket. It then automates their movement from one bucket to the next based on time passed and repayment activities. It also categorizes and labels borrowers who have more than one loan due. After the system has classified borrowers, managers can decide the correct collection strategy. It may include call, email, or reaching out through field agents.

A leading Indian bank’s secret to faster debt recovery (download here)!

A financial service firm holds multiple debtor profiles and a team of contact centers, field agents, and resolution agencies. Workflow automation tools within debt collection software handle distribution right from the start of inquiry to disbursal and collection. It automatically maps and distributes cases based on the availability of collectors, agents, and geographical location. Managers can also limit case allocation to ensure that collection agents work on high-priority debtors first. Especially in small businesses, where resources are limited, automation comes handy.

“One of our major concerns was missing out on cases or loan inquiries and it happened on a large scale. Workflow automation is a great relief since we can automatically distribute leads in a round-robin fashion based on our specifications.

Arif Hassan, Head – Customer Experience at Finnable

Accounts receivable management is a crucial aspect of the lending business. It involves tracking your customers at every stage of their lives. Knowing the actions of your clients on your website, e-mails, and other assets can trigger a task for collection teams. As soon as the debtor interacts with your message, the collection management software reciprocates the details in real-time. For example, when a debtor opens an email notice that has been sent by the lender, an automated collections system triggers an activity for the call-center team to follow-up with the debtor.

Notifications can bring to the debtor’s notice about the repayment date. But people classify frequent notifications as spam (73.47% of users who receive too many notifications, label them as spam). However, targeted in-app, WhatsApp notifications, SMS, or Emails can remind debtors for the date and time due for the installment and loan repayment.

A lender may involve a first-party or third-party collection agency for debt recovery. First-party collection agencies are usually subsidiaries of the lending company, whereas third-party collection agencies are not a part of the original company. Nevertheless, a lending company must keep a tab of collection agents/agencies to ensure timely debt recovery. Let us see how debt collection software simplifies this aspect as well.

With debt collection software, you can easily manage the complete call center lifecycle from the time of the first contact to repayment collection. For instance, based on call-center documents on the debtor’s dispositions, automated emails can be sent for urgent action. If there is no response from the debtor on the email, the system can automatically assign the case to a field collection agent. On the other hand, if a debtor attends to the agent’s call and promises to pay, a payment link can be sent via email or SMS. Collections CRMs also provide ready-to-use templates for SMS, emails, etc. which further improves the debt collection efficiency.

Collection software effectively manages field-agents’ productivity with reminder notifications, day planner, and route guidance to optimize their time on the field. Agents can achieve this via web-based or mobile lending CRM. Managers can track all field force activities and ensure productivity. Also, the feet-on-street collections agents can keep a tab on their pending tasks on their mobile app.

Watch the webinar recording: Digitizing Collections for faster debt recovery.

Debt collection software allows integration with CRMs, loan management systems, other in-house applications, and third-party apps such as IVR Telephony, Whatsapp Business API, to name some. Such integrations overcome the challenges of information silos.

“Knowlarity, our telephony service, is integrated with LeadSquared. Since the sales rep can view the complete customer history, data sharing over mails within internal teams has reduced by 60%, increasing efficiency, and security.”

Nitin Gupta, CEO & Co-founder, Finnable

QMS (Quality Management System) is a powerful tool to audit, measure, and improve the call quality via auto-selection logic (to select sample-recordings for audit per day) and auto-distribution logic (to avoid manual intervention). A custom-form scores each call-recording against multiple quality metrics. Then it generates an overall quality-score that acts as KPI (Key Performance Indicator) for the calling teams.

With this system, managers can identify the best and worst agents and define data-driven performance benchmarks. This is also helpful for training new agents with practical use cases.

Debt collection software analytics help decision-makers with data-driven insights on customers, collection efficiency, and team performances. These insights are crucial to evaluate ROI (Return on Investment) and eliminate bottlenecks from the collection funnel.

Smart analytics dashboards derive insights on borrower profiles, agent performances, active liabilities, pending payments, ongoing payment activities, and more. It also distinguishes cases based on a change in the lead stage and generates a performance report based on regions, agents, products, and teams.

The consolidated report covers the number of completed debt recoveries, intends to pay, non-responsive debtors, and the average time required for the debt recovery. With these reports, all the teams are in sync about the overall recovery performance – avoiding duplication of efforts. Thus, each stakeholder is aware of the defaulter’s stage of repayment.

Intelligent machine learning models can further predict the chances of recovery. Through automation and advanced analytics, you can assign recovery prediction scores to individual borrowers and the expected recovery time. This allows the management to take informed actions for individual cases and have a better contact strategy with the borrowers.

While you already have an idea of the features you need to look for in debt collection software, here are non-negotiable capabilities that the tool should have:

Pick software that can easily integrate with your existing CRM and account management systems in place. A rip-and-replace approach can be risky and can come with consequences like loss of data, a complete restructure of business operations, etc. Platforms, like LeadSquared, that are an end-to-end solution to digitize debt collection along with CRM capabilities are a good choice for fast-growing businesses.

If the user interface is complex and onboarding a user requires a significant chunk of time, it can hamper productivity and even cause errors down the line. So, the debt collection software that you choose should not just be easy to implement, but also easy to use.

As business requirements change based on the growth of the company, a scalable collections software that can adapt to these changes is crucial to improve the debt collection process. This could be in terms of case prioritization as more deals are processed, or in terms of analyzing a vast number of accounts to predict credit risk.

While a debt collection software needs to be user-friendly for internal purposes, its features must also enable better transparency and accessibility to the end-customers. This can include visibility into their loan payment journey, pending principal amount, and loan tenure details.

Most debt collection software come with an array of features that your business processes may not need. For example, for a growing company borrower management capabilities can be of great help whereas end-to-end call center management might not be useful. You need a tool that helps you pick and choose features and customize workflows based on your requirements.

In a nutshell, debt collection software eliminates dependencies on external institutions to a great extent by providing a panoramic view of cash flows and automating business processes. It gives you the flexibility to take charge of matters that are crucial to your business. Whether it’s keeping a tab on the inflow of money, ensuring security and compliance or being more data-driven, the bottom line is to maximize the effectiveness and impact of your processes for your end customers and internal teams.

Before we wrap up, here’s how our debt collections module helped ORIX Leasing & Financial Services:

“LeadSquared collections module helped us digitize our debt recovery process, building efficiencies and transparency. Also, tracking legal cases on the same module was a huge advantage.”

Harvinder Gandhi, Group Chief Information Officer, ORIX Leasing & Financial Services

To know more about how you can benefit from our collections CRM, book a personalized demo with us!

Debt collection software, also known as payment collection software, empowers lending organizations with end-to-end borrower management, recovery automation, and advanced analytics. It automates most of the aspects of the collection process.

Yes, many debt collection software integrates with ERP, loan management systems, and third-party apps.

You can use debt collection software to automate your collection process. View details.

The cloud-based collections software available for use on mobile is known as mobile lending CRM. Sometimes you will see both – responsive web application as well as a stand-alone mobile application for automating lending processes.

Enter your details and we'll send you a quick confirmation email to verify your address.

5 Ways to Improve Debt Collection Through Automation

5 Ways to Improve Debt Collection Through Automation