INSURANCE

Digital Insurance: Not an Option Anymore

Contents

The year 2020 has brought some unexpected changes in the insurance industry. While insurance was sold majorly through traditional channels like brokers and agents, COVID turned the spotlight on digital sales. The economic fallout altered the market trends by shifting focus on personalized premiums and simplifying products based on customer needs and expectations.

Listen to Mragendra Tomer, Head- Life Insurance, Paytm Insurance and Rajat Arora, VP – Marketing & Sales, LeadSquared, talk about the evolving landscape of Digital Insurance.

This article highlights the “digital-first” urgency in the insurance industry. But before we begin, let’s have a look at the insurance layout and what paved the way to its digital transformation.

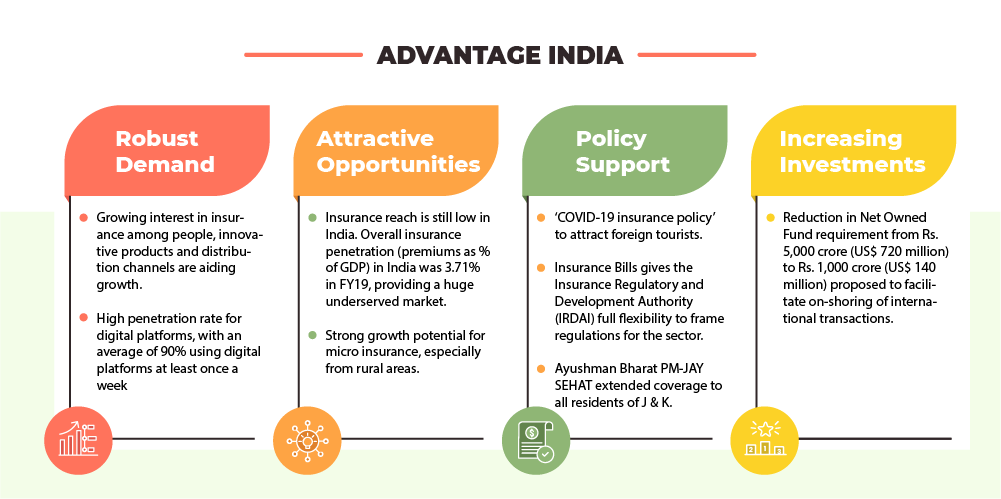

Insurance is one of the leading sectors in India contributing to the growth of the economy. Despite low insurance penetration in the country, the industry has been at an all-time high by the virtue of the number of premiums it collects and the scale of its investment. But, most fundamentally, it keeps growing due to the social and economic role it plays by covering personal and business risks.

The insurance industry of India currently has 57 insurance companies. Out of these 57, 24 are in the life insurance business, while 33 are non-life insurers. Where life insurance protects the livelihoods of individuals, general insurance, on the other hand, safeguards the GDP by protecting assets, businesses, health, and organizational reputation.

As per IRDAI, in 2009–10, the life insurance industry recorded a premium income of INR 2.65 lakh crore. But this increased to INR 5.1 lakh crore in 2018–19. On the other hand, the non-life insurance industry collected direct premiums worth INR 39,300 crore in 2009–10, which grew to INR 1.7 lakh crore in 2018–19. During the decade of 2009–2019, the life insurance industry collected a total of INR 35.26 lakh crore in premiums, while the non-life insurance industry collected INR 9.4 lakh crore as gross direct premiums.

As per a report by Oliver Wyman, 50% of the insurance agents think that COVID has led to a permanent acceleration in digital insurance purchasing.

The outbreak has affected the global insurance sector immensely. Insurance, which was seen as a push product, is now transforming into a pull product. Since the pandemic, people have become more concerned about their health and life. This change is leading to an increase in demand for insurance products.

During the Digital Insurance webinar, we ran a poll asking insurance professionals about their most productive sales channel in 2020.

54.55% of the respondents said that Telesales was the most productive channel, 45.45% said Point of Sales (POS), 22.73% said Feet-on-street (FOS), while the remaining 13.64% responded with Portfolio Management.

In line with the response, Mragendra Tomer, Head- Life Insurance, Paytm Insurance, says, “There is an ongoing transition from on-field to on-phone, which is imminent. It happened during COVID, and it will continue to remain. In the upcoming years, the demand for telesales will be more than that of field sales.“

The same sentiment is echoed across the larger business landscape.

Rajat Arora, VP – Marketing & Sales, LeadSquared, says, “At LeadSquared, sales was dominated by field force for many years. We started inside sales 3 months before the pandemic struck, and it was challenging to say the least. But we tried to figure out why people buy on the phone vs. face-to-face and discovered that you need to be very proactive while selling over the phone. Usually, these sales are fast-paced in nature like retail insurance, and if you can not bind the user in the first 2 minutes, then most likely there is no deal.“

Throughout the year 2020, digitization helped stabilize the growth of the insurance ecosystem. Every process from policy sales, marketing, documentation, claim processing, and customer onboarding relied on digital platforms. But the question is- Is digital insurance here to stay? Is digital insurance the new normal?

With digital transformation changing the dynamics of the industry, various manual processes have become digital. Operations are undergoing minor yet relevant changes to keep up with the growing consumer demands. Insurers are using customer journey builders and are integrating with various software to step up in their insurance selling game.

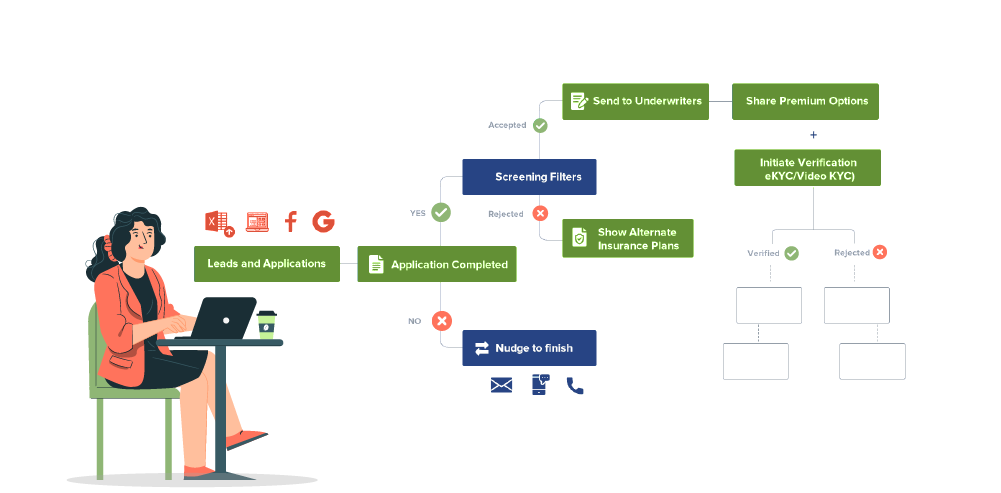

Anyone who has ever applied for insurance or filed a claim knows that it can be a long and daunting process. From underwriting to collections and every step in between, policy-holders feel like they’re running in loops.

Insurers can now solve this problem through Straight Through Processing. STP is a way of streamlining and simplifying the operations in the insurance industry. It enables the automated flow of information between systems.

While the STP crawls its way through the Insurance industry, it brings multiple benefits along with it. Using the method of Straight Through Processing, insurers can:

“The good thing about moving to digital is – Everything is trackable. And when you can track everything, there is a better chance of improving the sales journey,” says Rajat Arora.

The adoption of process automation in the insurance industry solves multiple challenges at once. Automation has now become a game-changing strategy to improve profit margins and streamline the overall operations dramatically.

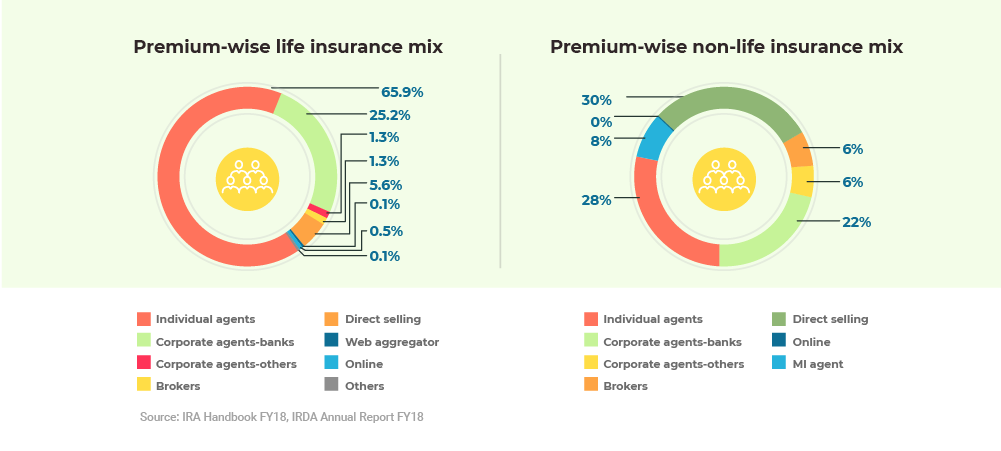

The insurance market relies heavily on on-field forces and intermediaries for distribution. But the pandemic has forced the customers to migrate online. Other channels of distribution like agents, brokers, banks, advisors are gradually shifting towards digital. Although the online channel existed before the pandemic, it wasn’t used to its full potential. The various ways to revamp the digital distribution channels are:

“Fixed Deposit is the most selling financial product to date. And the reason behind this is the simplification of the product. Brokers and agents are responsible for selling insurance to the consumer. Therefore, the product should not only be simple for the customer but also the agent or broker to understand so he can sell it further,” says Sourabh Lohtia, Director- Distribution Excellence, PNB MetLife.

The ways in which insurance products can be aligned with the customer needs are:

“If we talk about motor insurance, it is rather simple to understand and buy. Health insurance has also embraced digital. On the other hand, life insurance has gained traction but there is still scope for LI to grow further. Because of the technicalities involved, it is slightly difficult to understand and sell. Hence, insurers should look at ways to make it easier for the consumer to buy insurance without any assistance,” says Mragendra Tomer.

Insurers need to figure out to a way to reach their audience digitally. This includes embedding a phygital strategy – a hybrid of both physical and digital into the already existing Bancassurance model.

Insurance processes are known to be document heavy. Where motor insurance requires minimal documents, product like life insurance need various paperwork such as medical history, family history, habits, and more. Hence the documentation process needs to be simplified and this can be done by:

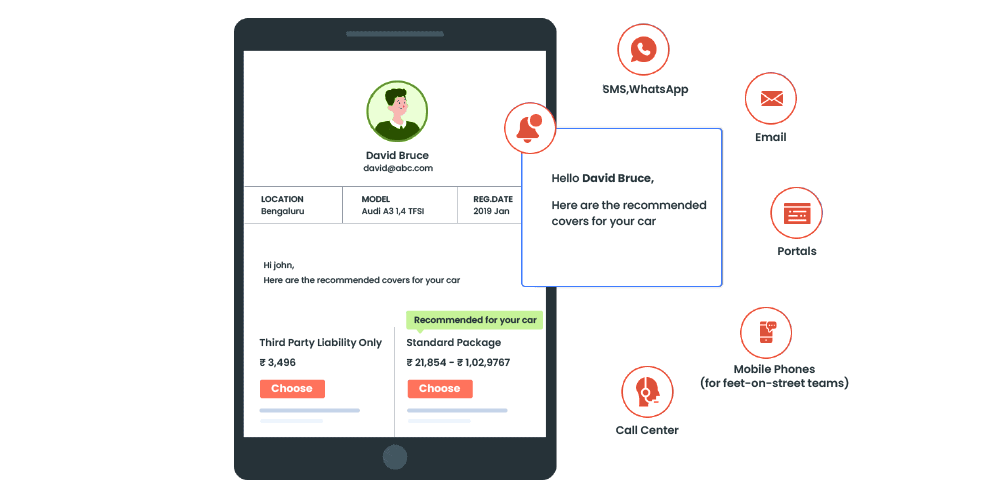

Omnichannel is not just about providing multiple platforms to the customer to interact. It’s about maintaining regular and personalized interaction with the end consumer across various channels. The following are the ways to successfully implement the omnichannel strategy:

A customer relationship management (CRM) is a tool that efficiently predicts customer behavior, ensures superior customer journey across various touch points, and gives a clearer picture of the sales funnel. An insurance agent or broker has various leads to work upon in a single day. And with increasing competition in the insurance sector, these leads can be lost within a blink of an eye if not attended on time.

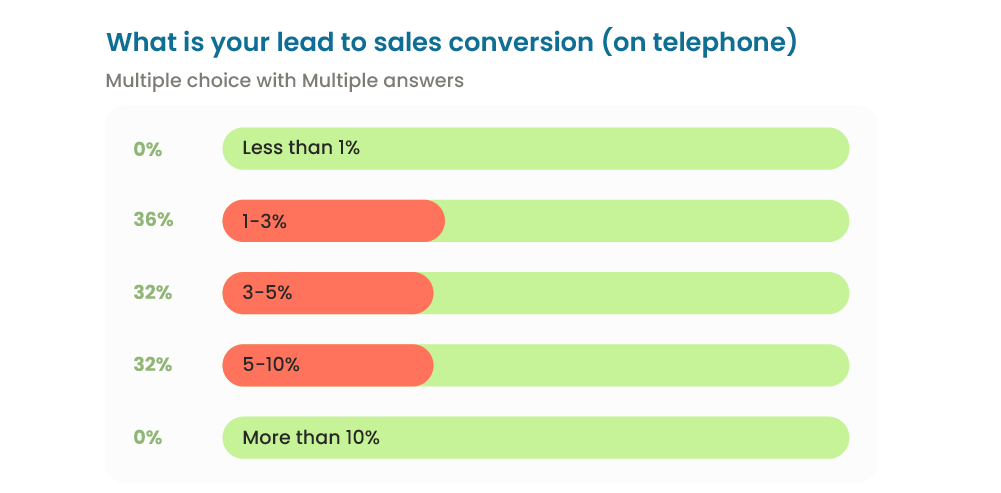

We asked the industry professionals – what is your lead to sales conversion rate on telephone?

36% of respondents believe their lead to sales conversion is 1-3%, 32% said 3-5%, another 32% agreed to 5-10% and no one opted for more than 10%.

With insurance gradually shifting to digital, a CRM tool has proven to improve the sales conversion ratio and shorten the company’s sales cycle without incurring much cost. The various features of a CRM tool that can effect your bottom line are:

Lead Management Systems have been in the market for almost 20 years. But they have evolved with the improving technology. A manager who is working from home can track his telesales team with just one click. He can see the number of calls made, the duration of the calls, deals in the pipeline, and more,” says Mragendra.

“Not just that, with telesales, the quality of conversation has improved since everything is trackable. So these are some of the benefits that come with digital transformation.”

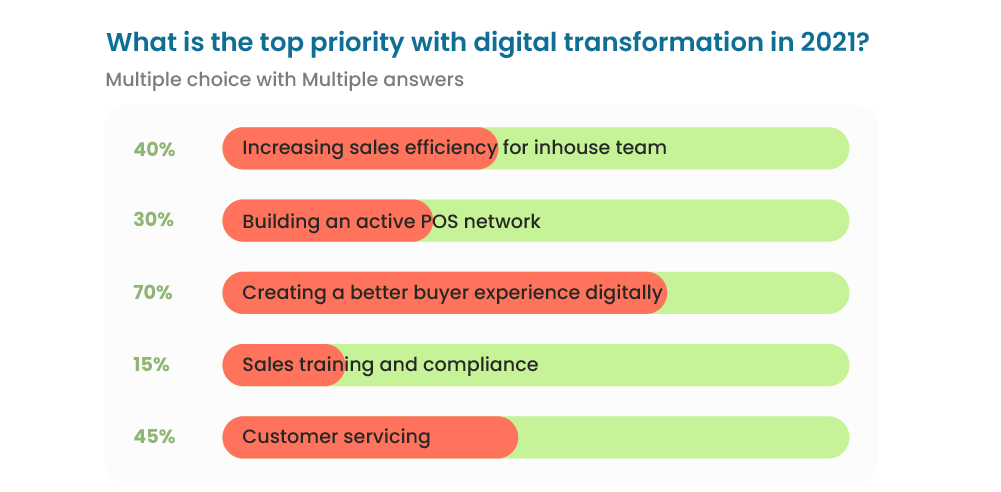

We asked the insurance professionals about their top priority for digital transformation in 2021.

70% of the respondents believe that creating a better buyer experience digitally is their top priority, 45% said customer training, 40% agreed on increasing sales efficiency for the in-house team, 30% said building an active POS network, and the remaining 15% responded with sales training and compliance.

With all major insurance processes moving to digital, insurers have witnessed a change in their business operations. Customer interactions have become better, processes have been streamlined, and agents and brokers can work faster and efficiently. The impact can be summarized in the below benefits:

Digital transformation in insurance is helping insurers to prepare for future challenges. With the Phygital model kicking in, companies are working on engaging with the customers via online and offline channels but with limited human interactions. New product innovations and integration with the right tools will help the insurance carriers improve customer experience and increase their revenue.

Business process efficiency is the biggest benefit of digital transformation. Following a digital process improves internal communication. And a well-informed team can help increase the company’s overall efficiency and further improve customer service. For instance, Artificial Intelligence, Machine Learning, and other technologies make claim processing and document collection simpler. AI chatbots assist customers with their queries and help insurers provide a better policy buying experience.

With increasing competition in the Insurance market, customers have several options to choose from. Hence, insurers need to drive the attention of the customer towards their product. Personalized communication with the consumer via his preferred platform helps the insurer stay competitive against digital disruptors. Analytical tools and marketing technology allow companies to trigger personalized campaigns to improve customer acquisition, retention, and ROI.

Digital Insurance is not an option anymore. It is here to stay!

The need of the hour is to have a seamless process in place, right from lead generation to follow up to medical underwriting and policy issuance with minimal physical dependencies. The future will see a shift from a product-centric approach to a customer-centric one. It will be shaped by new digital advancements, with social and peer-to-peer networking and smart devices all playing a part. By predicting customer behavior and utilizing this data in real-time, insurers can easily optimize their sales efforts. This way, consumers will also feel that their needs are understood and met in a “fast and convenient” way. It will eventually help in strengthening customer loyalty.

A dedicated CRM in the insurance sector performs many functions, but on top of the list is to foster healthy relationships between businesses and customers.

If you need help deciding on the perfect CRM for insurance companies, look no further. Check out LeadSquared Insurance CRM software.

In simple terms, digital transformation is fundamentally changing the industry-wide processes with technology. It helps in making the existing business process more efficient and improves customer service.

Technology trends like Robotic Process Automation (RPA), Artificial Intelligence (AI), and Machine Learning (ML) are changing the insurance industry rapidly. These trends allow the insurers to predict customer behavior, which helps them in creating tailor-made policies.

Enter your details and we'll send you a quick confirmation email to verify your address.

Credit Union Digital Marketing Strategies

Credit Union Digital Marketing Strategies