LENDING

Best lending business trends in 2026

Contents

Technology has been changing the financial services since the beginning of this decade. Facebook recently launched a digital currency of its own. Google announced a partnership with Citigroup. By the next decade, banking can look drastically different.

But the financial sector that is experiencing a dramatic shift is the lending business. With customers preferring digital-first platforms, financial institutions are scrambling to switch to digital. Also, financial institutions are now targeting Gen Z customers. The user base is now nearly 65 million in the United States (40% of total consumers). Soon, this digital-first population will become the primary customer base for financial institutions and there is no doubt that accommodating the new generation in legacy systems will be a challenge.

The 2022-23 lending trends involved lenders’ focus on matching borrowers’ expectations, leveraging omnichannel, and improving loan origination efficiency. Now, let us look at the lending business trends that will shape the industry in 2026.

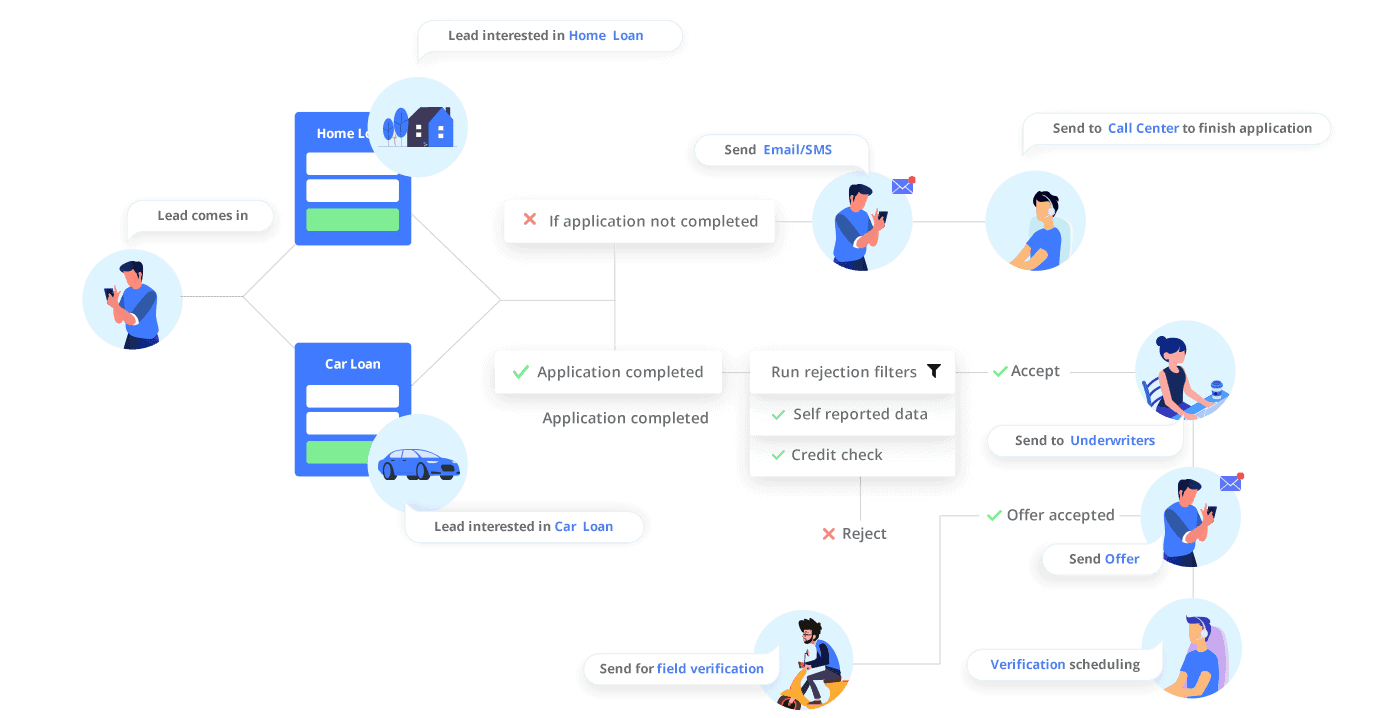

The most significant trend in lending will be increasing digitization. The switch will not happen instantly but will take place gradually. Digitization will allow banks and financial organizations to streamline their operations. These operations include customer information collection, organization, and analysis.

According to Accenture, over 50% of banking tasks are still manually performed. By using technology, banks in North America can save more than 70 billion USD through 2025. Automation can assist existing employees and increase the efficiency of financial organizations. Tech companies will also delve deeper into financial services. Automated platforms offer faster and more consistent credit approval. By using digital lending platforms, loan servicing takes much less time, and organizations can make decisions faster.

For starters, having the customer profile digitized is essential for easy access to customer information. Often, delays occur when relationship managers do not have access to relevant information. Having digital customer profiles also solves the issue of inconsistent or missing data.

Businesses can implement this using online application forms. This method is something younger generation will also prefer. All the relevant customer information, including their financial history, will be centrally stored. The entire credit team will have constant access to customer information. Thus, it will reduce delays in processing loans. Loan processors can use the information to sync up data from third-party firms.

Loan approval is one of the biggest bottlenecks in the lending business. Moreover, because of inconsistency in information between teams, errors are unavoidable – increasing business risks. Digital lending software provides an automated solution for the entire team. Digital platforms also provide a unified dashboard that keeps everyone on the same page. The dashboard will help lenders monitor customer interactions and reduce risks. Digitized solutions also provide back-end functions such as intelligence and analytics.

Loan management is still a paper-intensive process. Since accuracy is crucial in this business, a lot of manual labor goes into verifying documents. All steps – from loan application to disbursal and collection, involve manual work. The lending businesses that still rely on these legacy systems will need an extra push to digitize their operations.

For customers, digitization will bring convenience. They can apply for a loan with a few clicks. Lenders will also need to increase their response time by adopting automation. But automation may not always provide the desired outcome. In some cases, lenders may not get the results they want. The rush to replace legacy systems might cost them more in the long run. For this, the solution is to use integrative microservices. It allows lenders to digitize their operations at their own pace. The latest trend is cloud-based microservices. Companies can add these services as modules one by one. This system allows businesses to adapt to regulatory changes too.

For example, LeadSquared Lending CRM comes with pre-built integrations and data-exchange APIs to connect with multiple third-party apps like LOS, CIBIL, Experian Hunter, Perfios, NetBanking Connect, and PDF Statement Analyzer, to name some. It thus provides a one-stop solution to disburse loans faster.

Collaboration between banking and big tech has gained traction recently. Banks have been partnering with fintech for various services. For instance, NIBC bank is using the services of Oaknorth for credit analysis. It is an example of a collaborative model. Similarly, there exists a Point of Sale or POS transaction model. In this case, merchants can accept money using swipe machines. The aggregator model provides the consumer with all the lending options available. The peer-to-peer model allows consumers to borrow from many lenders who are willing to lend simultaneously.

[Also read: Retail lending – market opportunities and differentiator strategies]

The credit scoring systems of traditional banks are not suitable for SMEs. There is a lot of overhead with conventional scoring systems. SMEs often do not get access to credit because of this system. Some issues include extensive documentation, high-interest rates, and long decision-making times. Now, Fintechs are providing an alternative scoring system. They use data-driven models along with bank details.

These data points include:

Fintech also uses other data points, such as education level, degrees, and occupation. These alternative methods improve the accuracy of data-driven automated models. It eventually reduces the time and cost of servicing a loan. Thus, end customers can get funds with minimal effort.

Lending and Fintech partnerships will grow in the coming years. Lenders are willing to pair up with data providers, third party processors, and technology companies. The tie-ups will enable organizations to digitize their operations.

Moreover, Financial organizations will rely on the products and services from tech companies. The offerings include digital signing, fraud checking, credit scoring, ID verification, and video KYC. It will reduce manual labor to a great extent.

Technology will also replace numerous roles in the lending business. Organizations will have to restructure. Employees will have to upskill or reskill as lending will become more algorithmic.

Not everyone is fortunate enough to get financial aid in times of need. Banks often do not entertain small loans because of high underwriting costs and smaller profit margins. In the present economy, millennials often have little or no credit history. Therefore, these young adults often borrow from friends and family when they need financial aid.

Now, this is where the new lending businesses are coming into the picture. Fintech lending companies are offering “buy now pay later” loans. Consumers can get a product they want without having to fill out an extensive form. Moreover, these loans often have a zero-interest rate, and borrowers can even replay these loans as installments.

Borrowers can now get funds without having to visit the branch offices. Digital lending processes are chiefly self-serviced in nature. From applying for the loan to getting funds, the entire process needs little to no manual intervention. Customers will barely have to interact with the lender unless required. This automation also relieves the employees of redundant work.

Furthermore, digital lending also supports omnichannel communication – meaning that the customer can use any channel of their choice. They can communicate using the website, the app, text messages, or even social media platforms. Self-serve portals make lending businesses much more customer-centric.

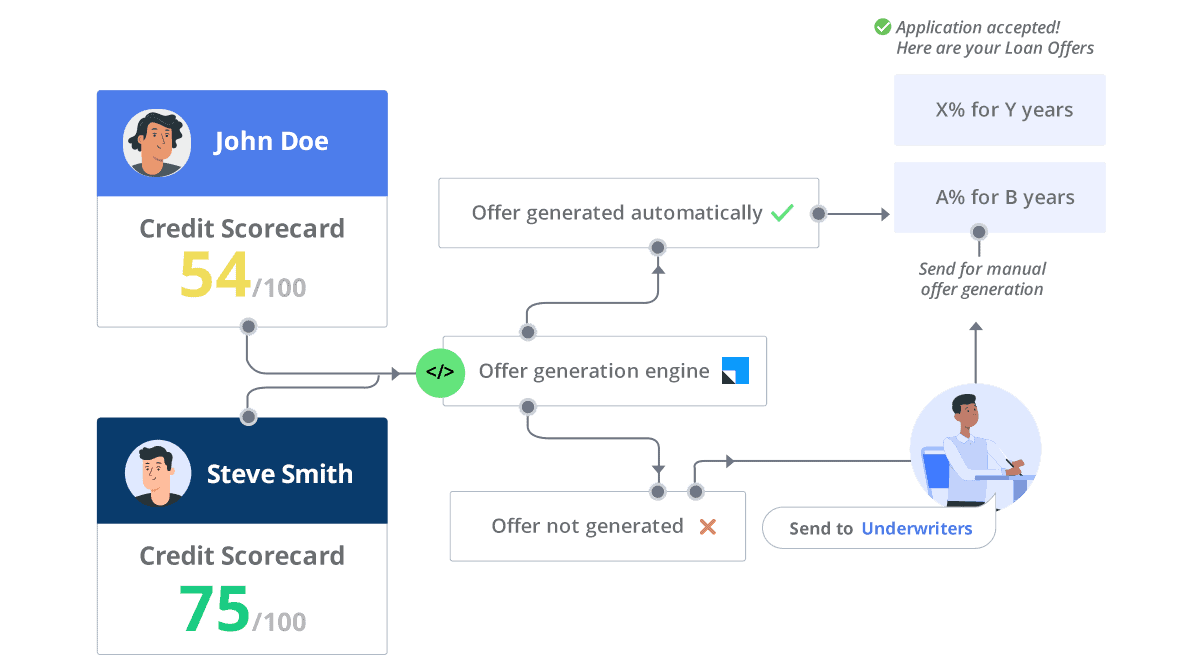

Machine learning and artificial intelligence are at the core of fintech. As ML and AI are progressing, fintech is incorporating them into more segments. Lenders are leveraging this technology to automate complex processes. Most of this is back-end work. ML and AI can help in checking for frauds, credit scoring, and automated loan offer generation.

We will see more applications of AI in the lending segment in the coming years.

Blockchain has been a groundbreaking technology for finances. The initial application of blockchain revolved around cryptocurrencies, but now it is helping improve financial products. Simply put, it is a shared, encrypted database – a distributed ledger. It makes the banking process faster and less bureaucratic. Blockchain is assisting in:

While traditional banking has reduced in-person communications, new-age lending businesses need zero. Consumers can interact with a simple digital interface. Mobile banking has already seen a massive increase. In the US, over three-quarters of the users prefer mobile baking. The digital interface is not just a form with menus and buttons. It can also be an intelligent and interactive chatbot. Customers no longer have to wait for human representatives to be free when they need help. It also reduces the workload of the employees without compromising on the quality of service.

Data and technology will dominate the future lending industry. Both consumers and financial institutions are embracing the change. Lending offers many opportunities in the current market. It is now more important than ever to improve the borrower experience. Complex compliance issues and regulations are here to stay, but digitization can simplify the process. To compete in 2026, lending businesses will have to digitize the loan lifecycle.

As lending becomes more digital, regulations are getting stricter. Lenders will rely on compliance-by-design technology, where regulatory checks are built directly into digital workflows. Automated KYC, AML checks, audit trails, and consent management will run in the background without slowing down loan processing. This allows lenders to move fast while staying compliant. Instead of manual audits and paperwork, regulators can review real-time data logs. For borrowers, this means quicker approvals without compromising data security or legal safeguards.

Traditional lenders often struggle with legacy systems, slower decision-making, and fragmented customer data. Fintech platforms, on the other hand, are digital-first and move faster. Banks that fail to modernize risk losing younger and small-business borrowers who value speed and simplicity. The biggest challenge will be cultural change—moving teams away from manual processes and rigid hierarchies. However, banks that adopt modular technology, partner with fintechs, and modernize customer experiences can still compete effectively while leveraging their trust and scale advantages.

As lenders collect more personal, behavioral, and financial data, customers are becoming more cautious about privacy. Trust will play a major role in choosing a lending provider. Borrowers will expect transparency about how their data is used and stored. Lenders that clearly explain consent, use secure encryption, and follow global data protection standards will gain an edge. Privacy-focused design—such as limited data sharing and user-controlled permissions—will help reduce fear and increase adoption, especially among first-time digital borrowers.

AI driven automation will not completely eliminate jobs, but it will significantly change roles. Repetitive tasks like data entry, document verification, and follow-ups will increasingly be handled by software. Lending employees will focus more on exception handling, customer relationships, risk analysis, and advisory roles. This shift makes upskilling essential. Institutions that invest in training their workforce will benefit the most. Automation reduces burnout and errors, while humans add judgment and empathy—both will be necessary for a balanced lending ecosystem.

Advanced lending technology is no longer limited to large banks. Cloud-based platforms and subscription pricing models make adoption affordable for smaller lenders. Instead of building systems from scratch, they can plug into ready-made tools for loan origination, analytics, and communication. Modular microservices allow lenders to start small and scale gradually. This approach reduces upfront costs while improving efficiency and customer experience. With the right technology choices, even small lenders can compete with larger players on speed, transparency, and service quality.

Digital identity verification has become essential as lending processes shift to online platforms. Lenders must confirm the identity of borrowers to prevent fraud and comply with regulatory requirements such as Know Your Customer (KYC) guidelines.

Modern verification systems use technologies like biometric authentication, document scanning, and facial recognition to confirm a borrower’s identity in real time. Video-based verification and AI-powered document analysis can also streamline onboarding processes while maintaining compliance.

By adopting digital identity solutions, lenders can significantly reduce onboarding time and eliminate the need for in-person verification. This not only improves efficiency but also enhances the overall borrower experience in fully digital lending environments.

Hyper-personalization involves using advanced data analytics and machine learning to tailor financial products and services to individual customers. Instead of offering generic loan options, lenders can analyze customer behavior, financial history, and preferences to recommend personalized loan products.

For example, a borrower with stable income and strong repayment history might receive customized interest rates or flexible repayment schedules. Similarly, personalized communication can guide customers through the loan application process and recommend relevant financial products.

This level of personalization enhances the borrower experience and increases the likelihood of successful loan conversions. It also strengthens customer loyalty by demonstrating that lenders understand and respond to individual needs.

Sustainability is becoming an important factor in financial services, including lending. Many financial institutions are incorporating environmental, social, and governance (ESG) considerations into their lending strategies.

For example, lenders may offer favorable financing terms for businesses that invest in renewable energy, green infrastructure, or sustainable manufacturing practices. Similarly, lenders are evaluating environmental risks when assessing large infrastructure or industrial projects.

Technology plays a role here as well. Data analytics tools help lenders evaluate sustainability metrics and assess how borrowers align with ESG standards. As regulatory bodies and investors increasingly prioritize sustainability, lenders will likely expand green lending initiatives and develop new financial products that support environmentally responsible projects.

Enter your details and we'll send you a quick confirmation email to verify your address.

22 Lead Conversion Strategies You Need to Adopt in 2026

22 Lead Conversion Strategies You Need to Adopt in 2026