LENDING

Bad Debt Recovery Strategies

Contents

Bad debt recovery is the money that your business receives after writing it off as uncollectable. The bad debt recovery process starts when the borrower cannot pay back the lender within the stipulated time. In this case, the lender may take legal action to recover the bad debt. The lender may recover the receivable as a partial payment or as equity. Bad debt recovery can also come by selling off the borrower’s collateral. For example, a borrower takes a car loan but fails to pay it back in time. In such a situation, the lender can repossess the car, sell it off and recover the loan.

From a lender’s perspective, debt recovery is challenging and cumbersome. Often the effort that goes into recovering a bad debt is not worth the repayment. However, in any case, the lending company must take certain actions before declaring a debt as bad debt. For instance, they can attempt in-house or third-party collection or even take legal actions. The collection efforts can still take place before the debt is declared bad.

If you see, payday loans, credit cards, and medical debt lead to the most unpaid loans in the US. As of 2018, 67% of payday loans caused bad debt. Since prevention is better than cure, preventing bad debts from happening in the first place is the best option for the lender.

Let us look at how financial institutions can reduce lending risks and improve collections.

The priority of any lending business should be to prevent bad debts from occurring at all. Therefore, lenders should know their borrowers well and if they can pay back the loan. Every time you give out a loan, you take a risk. Giving out loans to prime borrowers is easy. But when you want to expand your business and service to subprime customers, then the task becomes difficult.

For ages, traditional credit scores guided lenders. This scoring allowed both banks and lenders to disburse loans with confidence. Those who had lower scores required more time and evaluation. Lenders must go through multiple review processes to see if they can give the loan at all.

In lending business, declines are common. But there are also numerous exceptional cases. Banks, NBFCs, and other financial institutions can also give out loans conditionally. In these cases, just traditional credit scoring is not enough. Lenders must make use of relevant data and tools to judge the creditworthiness of subprime loan applicants. Rich applicant data and a consistent evaluation process are the keys to reducing lending risks.

There are numerous data sources available today that provide a much more detailed picture of an applicant’s financial health. In the digital banking world, these data sources are becoming increasingly important every single day. Fintech companies are allowing digital lending platforms to bank on these data sources when they make a decision.

Data privacy laws are crucial when companies collect customer data. The customer must legally agree to share their data, which includes sharing personal and confidential information. This data gives the companies a much clearer picture of the creditworthiness of the applicant. Alternative credit data may include:

Companies are now using alternative credit data for underwriting loans or using it to supplement existing credit scores. Almost 80% of lenders use at least one alternative credit data source. 16% of lenders plan to use data sources such as utility bill payments or rental payment records. Overall, lenders now rely on these data points to help assess borrowers better. This information assists lenders in making better decisions quicker.

Thin profiles can be both – a risk and an opportunity. Millions of US borrowers have thin profiles where it becomes difficult to assess creditworthiness.

(Source: https://onlinelibrary.wiley.com/doi/epdf/10.1111/ssqu.12389)

Thin profiles are those user profiles that have credit card accounts but haven’t used them actively. Or they may not be paying for several years. Those who use cash for purchases also have a thin profile because their purchase habits are not recorded. A thin profile gives an individual a bad credit score. However, this does not necessarily mean that the applicant is not eligible for a loan.

Dealing with thin profiles always poses a risk for the lender. In such cases, alternative credit scoring may be a solution. Unconventional data sources can indicate whether the individual qualifies for a loan. They can also show if there is considerable risk involved.

Alternative credit scoring data helps mitigate lending risks. But to make use of these data sources, lenders must digitize their processes. The combination of traditional credit data and alternative data can reveal numerous opportunities for lenders. Modern loan origination systems can help lenders decide if a borrower is creditworthy – in just a few minutes. Previously, the part of subprime applicants deemed unserviceable by banks or lenders can now qualify for loans using alternative data sources. Moreover, with this information, lenders can rule out high-risk applications.

Many loan origination systems offer out-of-box integration with alternative credit data sources. It is also possible to integrate other data sources using APIs. It consolidates data from different sources. All data is standardized. The system can then evaluate the creditworthiness or forward the consolidated data for manual underwriting. AI-assisted underwriting is a growing trend in the digital lending space. Borrowers can apply and get loans without any manual intervention from the lenders. However, borrowers should agree to share data that will allow the platform to assess their financial health.

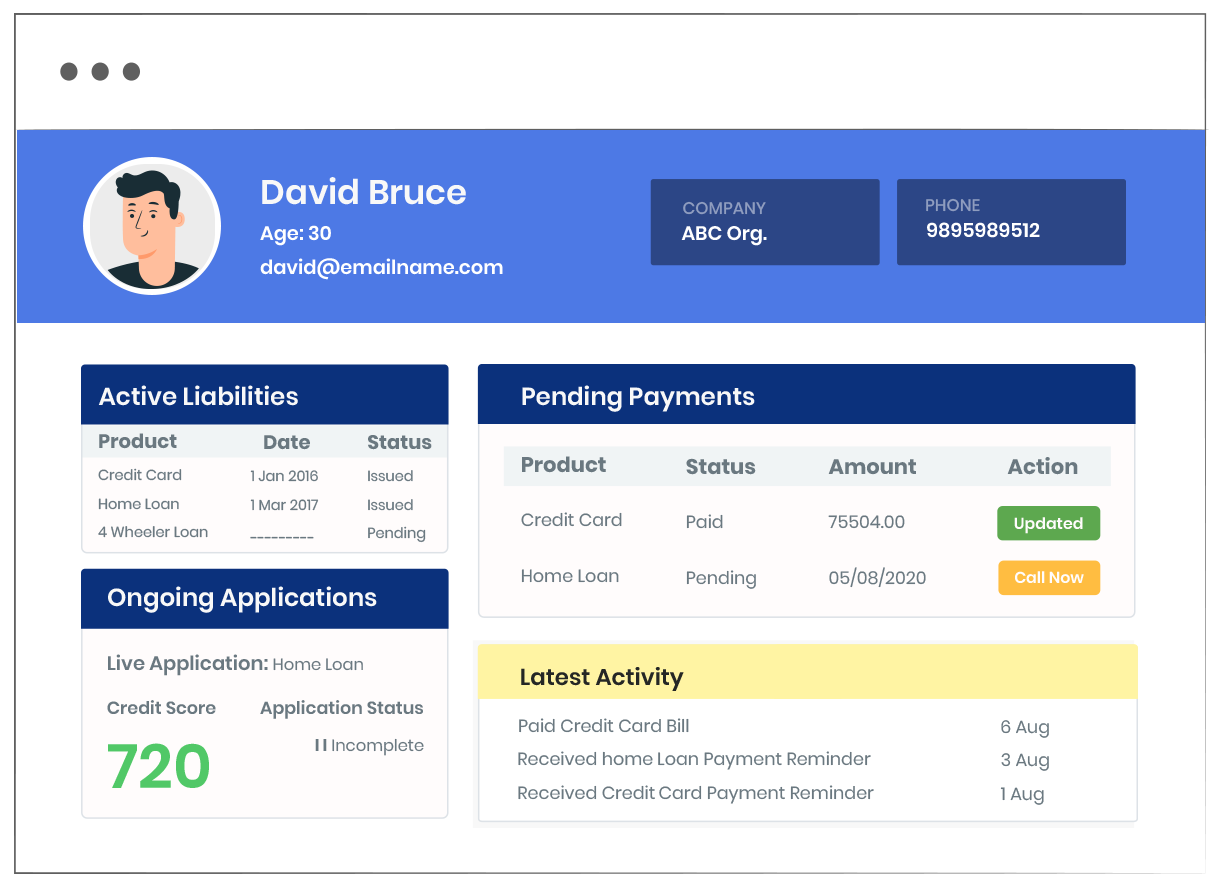

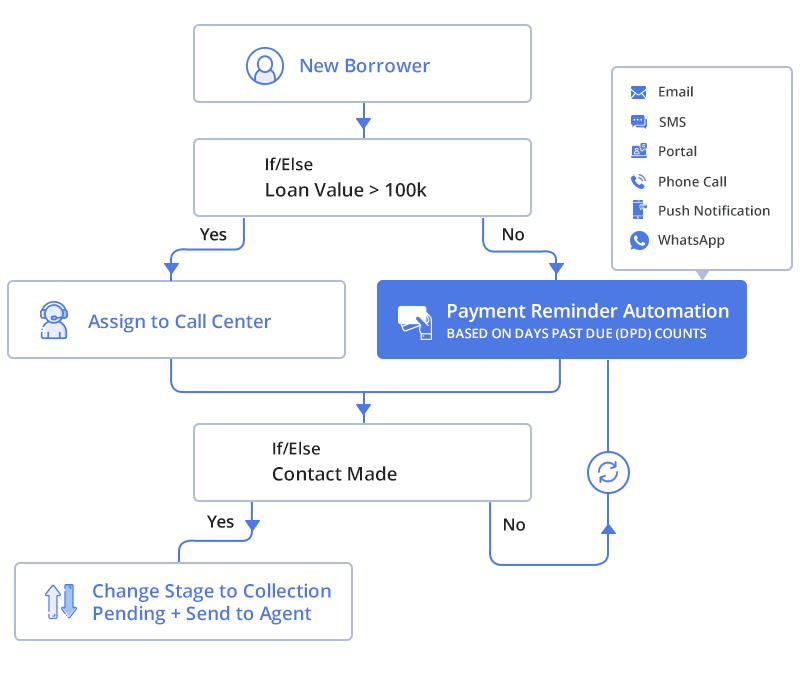

Timely collections help reduce bad debt and keeps the lending business in good health. While a loan origination system allows easy disbursement of loans to qualified applicants, a dedicated collections system encourages borrowers to pay on time. Lenders can make use of collections CRMs that can delegate borrowers to teams and agents automatically. For lending businesses, keeping track of borrowers can be challenging as the business grows. That is why CRM is a suitable option. A dedicated tool can also categorize borrowers and recommend collection strategies. It can remind agents to follow up with clients. It can also automate communications to debtors depending on their actions.

Dedicated loan origination systems allow businesses to analyze their portfolio performance regularly. This analysis enables companies to keep their underwriting processes efficient and accurate. For instance, some people with good traditional credit scores may show red flags when using alternative scoring. Some thin profile applicants may have a high risk associated with them. Some applicants without a FICO score may have a lower default rate than those with a low FICO score. These analyses can help you decide better when underwriting loans.

Bad debts are inevitable in lending businesses. No matter how careful you are, there may be situations when you need to declare debts as bad. Often, the borrower may face unforeseen circumstances for which they may not be able to pay even though they have good financial records. In any case, you will always want to recover the loan as much as possible and with as little effort as possible. Here are some steps which you can take to recover bad debts.

Not only is this a simple task, but in some regions, it is also a legal requirement. Before writing off debt as uncollectable, you need to send the borrower a letter. A collections CRM can automatically send an email based on DPD (Days Past Due). A hard copy letter exhibits the graveness of the situation much better. You can use a firm tone while expressing your intent to collect the payment.

A debt collection agency contacts debtors through phone calls and emails, and if necessary, through litigation. They persuade the debtors to pay the debt and often help them develop a payment plan. If required, a debt collection agency can assist the lender in filing a lawsuit. A debt collection agency works on a contingency agreement, where they keep a part of the amount they have recovered. A reliable agency knows how to properly communicate with debtors so that it does not destroy the lender’s relationship with its current client base.

Finally, you may want to investigate legal options if the insolvency is not addressed easily. However, you should note that a court case may not always go in your favor, and the entire process will incur court fees. Unless the amount is high, going to court may not be reasonable.

[Also read: Debt collection strategies for small businesses]

Alternative scoring and digital lending have changed the lending business landscape over the last few years. The massive amount of financial data and the software platforms that allow you to use that data make businesses much easier. It is now also much easier to serve subprime applicants. However, risks remain. Efficient usage of these tools can help mitigate risks and collect bad debts.

If you’re looking for digital solutions to streamline your lending operations, check out LeadSquared Collections CRM. You can also take a 15-day free-trial.

Effective bad debt recovery techniques include sending structured payment reminders, offering flexible repayment plans, negotiating settlements, engaging professional collection agencies, and using legal actions when necessary. Using automated collection systems can also help lenders track overdue payments and follow up consistently.

Lenders can reduce bad debt by improving credit assessment, analyzing borrower financial data, monitoring repayment behavior, and using automated risk scoring systems. A strong loan underwriting process helps identify high-risk applicants before approving loans.

Technology helps lenders automate payment reminders, track delinquent accounts, prioritize high-risk borrowers, and analyze collection performance. Modern collection platforms and CRMs can also help lenders manage borrower communication and improve recovery rates.

Legal action is typically considered when repeated payment reminders and collection attempts fail. If the outstanding amount is significant, lenders may file a lawsuit, enforce collateral recovery, or pursue court-approved settlements to recover the debt.

Enter your details and we'll send you a quick confirmation email to verify your address.

Digital Transformation in Education: Key Trends, Strategies, and Tips

Digital Transformation in Education: Key Trends, Strategies, and Tips