LENDING

Lending Business Strategy for New Age Digital Lenders

Contents

Several businesses are hard-hit by the effects of Covid-19. Financial instability is the norm, and borrowers have grown in number. Thus, doing business with the right borrower is essential for the success of your organization.

In this article, we’ll cover insights from KV Srinivasan, Executive Director and CEO of Profectus Capital, where he talks about how digital is transforming the lending business and making it easier to disburse loans. You can watch the webinar and hear him speak or read the takeaways below.

The earlier brick and mortar lending practices are shifting towards digitizing their operations. Digital lending is one of the fastest-growing fintech segments in India. It grew from nine billion U.S. dollars in 2012 to 110 billion dollars in 2019. Industry experts estimate that the digital lending market will reach a value of around 350 billion dollars by 2023.

Several organizations have started investing in technology that fosters growth. However, in current times, everyone can give similar turn-around-times for loan disbursal. It makes the existing established competitors hard to top and leaves only two areas of competition- pricing and customer service.

Pricing in the lending sector is a no-win situation. It has come down significantly in current times. In the past, lenders may have given a loan with an interest rate of 25%. But now it is at 6% in some places. Without a considerable profit margin, the business becomes unsustainable.

“At some point in time, the price competition has to stop. It will be a place of no return otherwise,” states KV Srinivasan.

Pricing as a point of competition exhausts the lender in the long run. Even if it is an area of competition, it causes unnecessary strain on lenders. Therefore, the more probable category of the competition is customer service.

The only way you can attract new customers and retain existing ones is to improve your service level. If you can understand customer expectations early, you are already a step ahead. Once you identify their intentions, you have your foot in the door. It will also increase the possibility of making a sale. So, what are the aspects of customer service that make a difference? Let’s take a look.

Tracking customers and their lifestyles enable the lender to identify points of lending. When you track your customers, you gain opportunities to cross-sell and upsell products. To elaborate on this, we can observe a simple parallel in the insurance sector.

Similarly, when you track your customer, you identify multiple opportunities to lend. Additionally, you can understand and meet their expectations based on their needs. For example, if you give a loan to a factory that purchases a machine, the machine itself may last for 5-6 years. As you are tracking them, you notice that their business has grown by 30% per year. It means that at some time when demand is high, they will need to buy another machine. They will take new loans for machinery in three cases-

In this manner, you can track an organization and its ups and downs and identify lending opportunities. Being a lender doesn’t mean you lend and leave. The idea behind tracking the customer’s life events is to build a lifelong relationship. However, tracking is one of the aspects that help you gain an edge against competitors. But tracking in itself requires something essential to succeed, which is data.

Lenders have always had data points to guide their decisions. Technology such as Lending CRM offers a 360-degree picture of consumers. You can collect data via multiple platforms, channels, products, and services. eKYC simplifies the customer verification process. You can receive a thorough analysis of someone’s bank statement in a matter of seconds. However,

Lending has evolved as more of a science than a pure art form. Earlier, you would assess the creditworthiness of a borrower through a conversation. Now, you can examine if they can repay or not by observing their credit history.

Customers seek personalization in all their purchasing decisions. By collecting relevant data, you can create products that are unique to your customer. So, the next step is to use data to understand their intent.

The substantial wealth of data is a boon in every lender’s organization. Predicting the failure of a business or a borrower is significantly easier. However, lenders face challenges due to a lack of understanding of customer intent. The intention to repay is much harder to know than assessing a borrower’s ability to repay. By looking at a borrower’s credit history, you can determine whether they can repay. But, you can only identify whether the person plans to pay after you have interacted with them. So, what are some ways one can delve into customer behavior and intent? Let’s see.

For example, by 2030, about 50% of Indian automobiles have to be electric. What does that mean for the automobile sector? Or the auto-component sector?

A massive change will take place due to the change in engines. Electrical engines will boost business for companies that create electric components. But it will also bring down the number of diesel and oil-based engines.

So, understand the market and trends and create products that will cater to the auto-sector of tomorrow and not the auto-sector of yesterday.

“Create industry-related products, keeping in mind the future of the industry you are selling to,” says KV Srinivasan.

Ultimately, understanding intent falls under the art of lending. You can only know what your customer’s intentions are once you converse with them. Three points to keep in mind when trying to assess the borrower’s intent-

Finding creditworthy borrowers generally depends on the customer’s credit history. But that’s only one part of the process. Understanding their intent is what brings you closer to successful sales. Now coming to the final aspect of lending to the worthy, that is personalization.

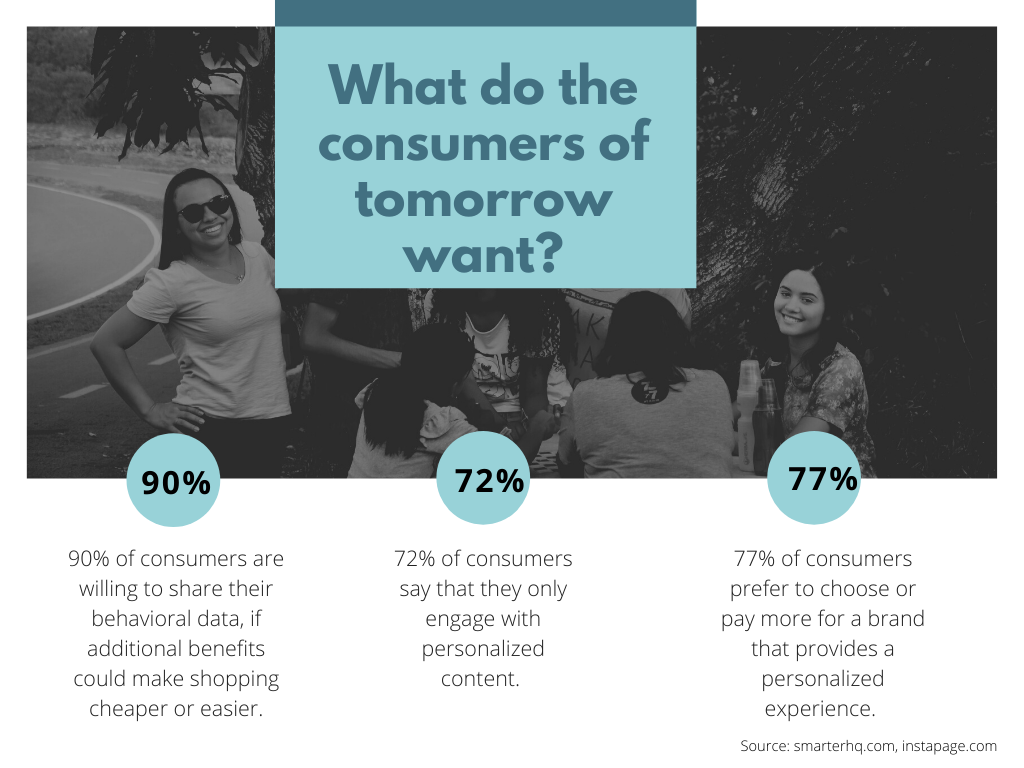

Each customer is different. So, if you can create something unique to them, they are bound to buy it – even at a higher price. A generic package that applies to everyone satisfies only a part of your customer’s needs. Instead, create a personalized product and give your customer 100% satisfaction. Research shows that consumers of tomorrow want the following:

Once you collect data about your customer, you can use it to cater to their needs. Let’s look at an example to understand how personalization can make a difference.

So, these were some of the ways to find borrowers and serve their needs. However, there is one final aspect to build credibility and a strong relationship.

In a borrower’s mind, transparency trumps low prices. Lenders need to be as honest as possible when interacting with customers. 89% of consumers have switched to a competitor after a poor customer experience. And these negative experiences are often caused by a lack of transparency. Let’s imagine a scenario that creates a negative impression and how to remedy it.

Both scenarios will irritate and push your customer to a competitor. The way to fix this is by conveying what exactly you can do. When there is a problem, communicate it as soon as possible. Communicating any issue ensures that you won’t be letting your customer down. Instead, your customer will appreciate your level of honesty and service standards. The best method to ensure transparency is education.

Your sales reps need the right tools to interact with customers effectively. A tool that tracks, records, notifies, and reminds them is essential. Once you provide them with the right tools, such as Lending CRM, positive customer experiences will follow.

Every customer deserves experiences that are positive and enriching. Lenders must not only be fair-weather friends. But instead, they must hold the borrower’s hand when their chips are down. In India, financial inclusion is low, making transparency and reaching borrowers difficult.

But this also means that there is immense growth opportunity in the lending sector. The number of internet users has also increased exponentially. Currently, India encompasses 624.0 million internet users as of 2021. You must establish a digital procurement system to reach those in need.

The lending businesses face challenges due to a lack of understanding of customer intent. It is difficult to assess whether a borrower will repay a loan just by looking at their credit history. Businesses can improve their chances of success by understanding customer intent through interacting with the borrower.

Lending businesses can use technology in a few ways to overcome challenges like tracking customer life events and lifestyles to identify points of lending and cross-sell products. They can also utilize Lending CRM to gain a 360-degree view of consumers. This can include data collection via multiple platforms, channels, and products.

Also, analyze a borrower’s credit history to determine if they can repay a loan.

Understanding customer intent is key to success. In order to assess this, lenders should collect data on their customers and track their life events. This data can be used to predict their needs and offer them personalized loan products. However, lenders also need to ensure they are transparent with their customers.

KV Srinivasan

Executive Director & CEO

Profectus Capital

An alumnus of the Indian Institute of Management, Ahmedabad (1989), KV Srinivasan is also a member of the Institute of Chartered Accountants of India (1985) and Institute of Company Secretaries of India (1987). Having worked with ICICI Prudential Life Insurance, ITC Classic Finance, Reliance Life Insurance, and Reliance Commercial Finance, Srinivasan has over three decades of experience in the BFSI sector. Srinivasan is the Director of the Finance Industry Development Council. He is also the Co-Chairman of the NBFC Committee of IMC Chamber Of Comme

Enter your details and we'll send you a quick confirmation email to verify your address.

A Handy Guide to Sales and Operations Planning (S&OP)

A Handy Guide to Sales and Operations Planning (S&OP)