https://www.leadsquared.com/wp-content/uploads/2021/11/Mobile-Marketing-1.jpg400800Padma Ramakrishnahttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Padma Ramakrishna2021-03-31 21:27:062023-04-17 18:35:15Credit Union Digital Marketing Strategies

https://www.leadsquared.com/wp-content/uploads/2021/11/Mobile-Marketing-1.jpg400800Padma Ramakrishnahttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Padma Ramakrishna2021-03-31 21:27:062023-04-17 18:35:15Credit Union Digital Marketing Strategies https://www.leadsquared.com/wp-content/uploads/2021/11/digital-insurance.png4501001Diksha Sharmahttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Diksha Sharma2021-03-31 10:34:192024-03-06 22:50:52Digital Insurance: Not an Option Anymore

https://www.leadsquared.com/wp-content/uploads/2021/11/digital-insurance.png4501001Diksha Sharmahttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Diksha Sharma2021-03-31 10:34:192024-03-06 22:50:52Digital Insurance: Not an Option Anymore https://www.leadsquared.com/wp-content/uploads/2021/11/Agency-management-system.jpg5541000Diksha Sharmahttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Diksha Sharma2021-03-30 13:17:242023-03-03 13:26:43Insurance Agency Management System – What, Why, and How?

https://www.leadsquared.com/wp-content/uploads/2021/11/Agency-management-system.jpg5541000Diksha Sharmahttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Diksha Sharma2021-03-30 13:17:242023-03-03 13:26:43Insurance Agency Management System – What, Why, and How? https://www.leadsquared.com/wp-content/uploads/2022/04/Artboard-1.png5001000Shibani Royhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Shibani Roy2021-03-26 13:45:002022-12-27 21:52:50[Webinar] How University Admissions Have Pivoted Post Covid

https://www.leadsquared.com/wp-content/uploads/2022/04/Artboard-1.png5001000Shibani Royhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Shibani Roy2021-03-26 13:45:002022-12-27 21:52:50[Webinar] How University Admissions Have Pivoted Post Covid https://www.leadsquared.com/wp-content/uploads/2021/11/MSME-lending-market-opportunity-and-differentiator-strategy.jpg4501000Nidhi Agarwalhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Nidhi Agarwal2021-03-23 18:20:282023-12-13 18:11:11MSME Lending Market Trends 2024

https://www.leadsquared.com/wp-content/uploads/2021/11/MSME-lending-market-opportunity-and-differentiator-strategy.jpg4501000Nidhi Agarwalhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Nidhi Agarwal2021-03-23 18:20:282023-12-13 18:11:11MSME Lending Market Trends 2024 https://www.leadsquared.com/wp-content/uploads/2021/11/15-tips-for-agent-productivity-Hero-Image.png4501000Mayankhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Mayank2021-03-22 10:25:412023-12-14 15:23:1215 Tips for Real Estate Agents and Developers

https://www.leadsquared.com/wp-content/uploads/2021/11/15-tips-for-agent-productivity-Hero-Image.png4501000Mayankhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Mayank2021-03-22 10:25:412023-12-14 15:23:1215 Tips for Real Estate Agents and Developers https://www.leadsquared.com/wp-content/uploads/2021/11/neobanks-growth-and-profitability-strategy.jpg4501000Nidhi Agarwalhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Nidhi Agarwal2021-03-18 18:20:482023-12-11 14:50:31Neobanks of the Future

https://www.leadsquared.com/wp-content/uploads/2021/11/neobanks-growth-and-profitability-strategy.jpg4501000Nidhi Agarwalhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Nidhi Agarwal2021-03-18 18:20:482023-12-11 14:50:31Neobanks of the Future https://www.leadsquared.com/wp-content/uploads/2021/11/banking-chatbot-customer-experience.jpg4501000Jiaqi Panhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Jiaqi Pan2021-03-17 18:05:372023-12-21 14:47:21Banking Chatbot: 5 Ways It Helps

https://www.leadsquared.com/wp-content/uploads/2021/11/banking-chatbot-customer-experience.jpg4501000Jiaqi Panhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Jiaqi Pan2021-03-17 18:05:372023-12-21 14:47:21Banking Chatbot: 5 Ways It Helps https://www.leadsquared.com/wp-content/uploads/2021/11/retail-lending-market-opportunity-and-differentiator-strategy.jpg4501001Nidhi Agarwalhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Nidhi Agarwal2021-03-16 19:26:192023-12-15 15:14:28Retail Lending Market Opportunities in 2024

https://www.leadsquared.com/wp-content/uploads/2021/11/retail-lending-market-opportunity-and-differentiator-strategy.jpg4501001Nidhi Agarwalhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Nidhi Agarwal2021-03-16 19:26:192023-12-15 15:14:28Retail Lending Market Opportunities in 2024 https://www.leadsquared.com/wp-content/uploads/2021/11/insurance-online-and-offline-distribution-channels.png4511001Diksha Sharmahttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Diksha Sharma2021-03-15 23:11:032022-12-28 14:23:03Streamlining Online and Offline Insurance Distribution Channels

https://www.leadsquared.com/wp-content/uploads/2021/11/insurance-online-and-offline-distribution-channels.png4511001Diksha Sharmahttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Diksha Sharma2021-03-15 23:11:032022-12-28 14:23:03Streamlining Online and Offline Insurance Distribution Channels https://www.leadsquared.com/wp-content/uploads/2021/11/Landing-Page-vs-Home-Page-1.jpg363680Meenu Joshihttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Meenu Joshi2021-03-14 09:57:212023-12-21 15:45:25How We Increased Sign-ups by 39% With These Landing Page Design Hacks

https://www.leadsquared.com/wp-content/uploads/2021/11/Landing-Page-vs-Home-Page-1.jpg363680Meenu Joshihttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Meenu Joshi2021-03-14 09:57:212023-12-21 15:45:25How We Increased Sign-ups by 39% With These Landing Page Design Hacks https://www.leadsquared.com/wp-content/uploads/2021/11/EduTech-Trends-Interactive-video-and-media.jpg5001000Vivek Hariharanhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Vivek Hariharan2021-03-12 18:50:142023-12-11 10:41:50EduTech: New Technologies in the Education Sector

https://www.leadsquared.com/wp-content/uploads/2021/11/EduTech-Trends-Interactive-video-and-media.jpg5001000Vivek Hariharanhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Vivek Hariharan2021-03-12 18:50:142023-12-11 10:41:50EduTech: New Technologies in the Education Sector https://www.leadsquared.com/wp-content/uploads/2021/11/B2B-vs-B2C-marketing-differences-and-similarities.jpg6021000Nidhi Agarwalhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Nidhi Agarwal2021-03-12 10:05:562023-12-13 15:53:24B2B vs B2C Marketing: 10 Key Differences

https://www.leadsquared.com/wp-content/uploads/2021/11/B2B-vs-B2C-marketing-differences-and-similarities.jpg6021000Nidhi Agarwalhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Nidhi Agarwal2021-03-12 10:05:562023-12-13 15:53:24B2B vs B2C Marketing: 10 Key Differences https://www.leadsquared.com/wp-content/uploads/2021/11/enrollment-letters.jpg417626Sarilya Jaiswalhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Sarilya Jaiswal2021-03-11 02:57:162022-12-27 15:45:42[Webinar Recording] The Love Letters of Enrollment

https://www.leadsquared.com/wp-content/uploads/2021/11/enrollment-letters.jpg417626Sarilya Jaiswalhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Sarilya Jaiswal2021-03-11 02:57:162022-12-27 15:45:42[Webinar Recording] The Love Letters of Enrollment https://www.leadsquared.com/wp-content/uploads/2021/11/RealEstateSalesStrategy-Image-1.png9392084Mayankhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Mayank2021-03-10 14:40:012023-12-13 18:33:14Residential Real Estate Sales Strategy for 2024

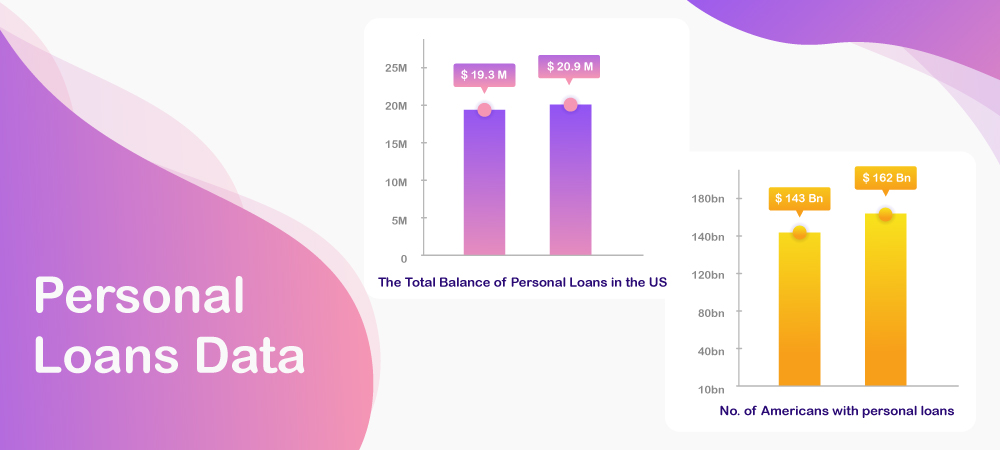

https://www.leadsquared.com/wp-content/uploads/2021/11/RealEstateSalesStrategy-Image-1.png9392084Mayankhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Mayank2021-03-10 14:40:012023-12-13 18:33:14Residential Real Estate Sales Strategy for 2024 https://www.leadsquared.com/wp-content/uploads/2021/03/Personal-Loans-Data-1.jpg4501000Padma Ramakrishnahttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Padma Ramakrishna2021-03-09 16:29:242023-12-16 22:30:39Consumer Lending Trends 2024

https://www.leadsquared.com/wp-content/uploads/2021/03/Personal-Loans-Data-1.jpg4501000Padma Ramakrishnahttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Padma Ramakrishna2021-03-09 16:29:242023-12-16 22:30:39Consumer Lending Trends 2024 https://www.leadsquared.com/wp-content/uploads/2021/11/sales-opportunity-management-and-best-practices.jpg5321000Nidhi Agarwalhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Nidhi Agarwal2021-03-09 09:32:182023-01-02 19:40:08Sales Opportunity Management Best Practices

https://www.leadsquared.com/wp-content/uploads/2021/11/sales-opportunity-management-and-best-practices.jpg5321000Nidhi Agarwalhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Nidhi Agarwal2021-03-09 09:32:182023-01-02 19:40:08Sales Opportunity Management Best Practices https://www.leadsquared.com/wp-content/uploads/2021/11/Edtech-expert-sales-strategy.jpg5001000Vivek Hariharanhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Vivek Hariharan2021-03-05 19:08:162024-03-20 17:33:44The Expert Strategy for Scaling Sales in EdTech

https://www.leadsquared.com/wp-content/uploads/2021/11/Edtech-expert-sales-strategy.jpg5001000Vivek Hariharanhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Vivek Hariharan2021-03-05 19:08:162024-03-20 17:33:44The Expert Strategy for Scaling Sales in EdTech https://www.leadsquared.com/wp-content/uploads/2021/11/what-is-lead-and-opportunity-management.jpg5801000Nidhi Agarwalhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Nidhi Agarwal2021-03-04 18:21:252023-12-21 16:14:02Difference Between Lead and Opportunity Management

https://www.leadsquared.com/wp-content/uploads/2021/11/what-is-lead-and-opportunity-management.jpg5801000Nidhi Agarwalhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Nidhi Agarwal2021-03-04 18:21:252023-12-21 16:14:02Difference Between Lead and Opportunity Management https://www.leadsquared.com/wp-content/uploads/2021/11/Feature-Image_PropTech.png4501000Mayankhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Mayank2021-03-01 10:24:192023-12-21 16:27:42PropTech: A Digital Revolution in Real Estate

https://www.leadsquared.com/wp-content/uploads/2021/11/Feature-Image_PropTech.png4501000Mayankhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Mayank2021-03-01 10:24:192023-12-21 16:27:42PropTech: A Digital Revolution in Real Estate https://www.leadsquared.com/wp-content/uploads/2021/11/door-to-door-sales-app.jpg5001000Nidhi Agarwalhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Nidhi Agarwal2021-03-01 08:10:002023-11-02 16:38:31Door-to-door Sales App (Mobile CRM)

https://www.leadsquared.com/wp-content/uploads/2021/11/door-to-door-sales-app.jpg5001000Nidhi Agarwalhttps://www.leadsquared.com/wp-content/uploads/2023/12/340-x-156-300x138-1.png Nidhi Agarwal2021-03-01 08:10:002023-11-02 16:38:31Door-to-door Sales App (Mobile CRM)